You can Download Chapter 1 Accounting for Partnership : Basic Concepts Questions and Answers, Notes, 2nd PUC Accountancy Question Bank with Answers Karnataka State Board Solutions help you to revise complete Syllabus and score more marks in your examinations.

Karnataka 2nd PUC Accountancy Question Bank Chapter 1 Accounting for Partnership : Basic Concepts

2nd PUC Accountancy Accounting for Partnership : Basic Concepts NCERT Textbook Questions and Answers

2nd PUC Accountancy Accounting for Partnership : Basic Concepts Short Answer Type Questions and Answers

Question 1.

State the meaning of Not-for-profit organizations.

Answer:

Not-for-profit organizations refers to the organizations that are used for the welfare of the society and are set up as charitable institutions which function without any profit motive.

Question 2.

State the meaning of Receipts and Payments Account.

Answer:

Receipt and payment account is the summary of cash and bank transactions which helps in the preparation f income and expenditure account and the balance sheet.

Question 3.

State the meaning of Income and Expenditure Account.

Answer:

It is the summary of income and expenditure for the accounting year. It is like a profit and loss account prepared on accusal basis in case of the business organization.

Question 4.

What are the feature of Receipts and Payments Account?

Answer.

- It is a summary of cash book.

- It shows the total amounts of all receipt and payments irrespective of the period to which they pertain.

- It includes all receipts and payments whether they are of capital nature and or of revenue nature.

![]()

Question 5.

What steps are taken to prepare Income and Expenditure Account from a Receipts and Payments account?

Answer:

- Pursue the receipts and payments account throughly.

- Exclude the opening and closing balances of cash and bank as they are not an income.

- Exclude capital receipts and capital payments as these are to be shown in the balance sheet.

- Consider only the revenue receipts to be shown on the income side, and revenue expenditure to the expenditure side of the income and expenditure account.

- Considering the following items not appearing in the receipts and payments account that need to be taken into account for determining the surplus deficit for current year:

- Depreciation of fixed assets:

- Provision for doubtful debts if required

- Profit or loss on sale of fixed assets.

Question 6.

What is subscription? How is it calculated?

Answer:

Subscription is a membership fees paid by the member on annual basis. Its is calculated by taking current year subscription plus receivables and deducted previous year and next year subscription and balance amount treated as subscription for the year.

Question 7.

What is capital fund? How is it calculated?

Answer:

It consists of Capitalized receipts such as Legacies, Life membership fees, Entrance fees, and Donation for the current year and excess of income over expenditure of the current year. Capital fund is the difference between the assets and liabilities of non-profit organization.

2nd PUC Accountancy Accounting for Partnership : Basic Concepts Long Answer Type Questions and Answers

Question 1.

Explain the statement: “Receipt and Payment Account is a summarised version of Cash Book”.

Answer.

It is prepared at the end of the accounting year on the basis of cash receipts and cash payments recorded in the cash book. It simply is a summary of cash and bank transactions under various heads. Receipt and Payment Account gives summarised picture of various receipts and payments, irrespective of whether they pertain to the current period, previous period or succeeding period or whether they are of capital or revenue nature. It may be noted that this account does not show any non-item like depreciation.

The opening balance in Receipt and Payment Account represents cash in hand/ cash at bank which is shown on its receipts side, and the closing balance of this account represents cash in hand and bank balance as at the end of the year, which appear on the credit side of the Receipt and Payment Account.

Question 2.

“Income and Expenditure Account of a Not-for-Profit Organisation is akin to Profit and Loss Account, of a business concern”. Explain the statement.

Answer:

It is the summary of income and expenditure for the accounting year. It is just like a profit and loss account prepared on accrual basis in case of the business organisations. It includes only revenue items and the balance at the end represents surplus or deficit. The Income and Expenditure Account serves the same purpose as the profit and loss account of a business organisation does.

All the revenue items relating to the current period are shown in this account, the expenses and losses on the expenditure side and incomes and gains on the income side of the account. It shows the net operating result in the form of surplus (i.e. excess, of income over expenditure) or deficit (i.e. excess of expenditure over income), which is transferred to the capital fund shown in the balance sheet.

Question 3.

Distinguish between Receipts and Payments Account and Income and Expenditure Account.

Answer:

| Receipts and Payments A/c | Income and Expenditure A/c |

| (i) It is a real account. | (i) It is a nominal account. |

| (ii) It is prepared from the cash book. | (ii) It is prepared from the receipts and payments and other information. |

| (iii) It is on the basis of actuals Receipts and Payments and not considered accruals. | (iii) In this statement accruals of Receipts and Payments considered. |

| (iv) The different treated as cash balance or bank balance. | (iv) The different treated as profit or deficit for the year. |

Question 4.

‘Explain the basic features of Income and Expenditure Account and of Receipts and Payments

Account.

Answer.

The Basic features of Receipts and Payments Accounts are :

- It is a summary of a simple cash book.

- It shows the total amounts of all receipts and payments irrespective of the period to which they pertain.

- It includes all receipts and payments whether they are of capital nature or of revenue nature.

- No distinction is made in receipts/payments made in cash or through bank. With the exception of the opening and closing balances, the total amount of each receipts and payments is shown in this account.

- No non-cash items such as depreciation outstanding expenses accrued income, etc. are shown in this account.

The basic features of Income and Expenditure Account are

- It is a nominal account.

- It is prepared from the receipts and payments and other information.

- In this statement accruals of Receipts and Payments considered.

- The different treated as profit or deficit for the year.

Question 5.

Show the treatment of the following items by a not-for-profit organization:

(i) Annual subscription

(ii) Specific Donation

(iii) Sale of Fixed Assets

(iv) Sale of old periodicals

(v) Sale of Sports Materials

(vi) Life Membership Fee

Answer:

(i) Annual subscription :

- Actual subscription received during an accounting year are shown on debit side of receipts and payment a/c.

- Later subscription transfered to income and expenditure account to the extent of current year amount. Such transfer shown on credit side of inc.ome and expenditure a/c

- Subscription received, which is related to previous year should deducted from balance sheet assets side amount shown.

- Subscription received for next year should be shown an balance sheet liabilities side as received in advance.

- Subscription due but not received should be added to subscription received on income and expenditure a/c credit side and the same to be shown on assets side of the balance sheet under‘Receivables or amount due but not received’.

(ii) Specific donation – The fund received for specific purpose From the donors called special funds or special donation. The accounting treatment of special donation:-

- Amount received as specific donation should be shown on receipts side or debit side of receipts and

- Specific donation capital receipts in its nature so it should be shown on balance sheet liability side.

- Any payment made for that specific purpose to that extent should deduct from balance of amount shown in previous year balance sheet.

- Any amount received during the year should added to previous year balance amount.

(iii) Sale of fixed assets – The assets in the business should be sale for many reasons. In case of such sales doing the year, the accounting treatment is as follows.

- Sale of assets is the receipt such receipt should be shown on debit side of receipt and payment a/c.

- Sale of assets receipt is a capital receipt. The book value should be deducted from the existing assets balance.

- In case of any loss on sale of fixed assets should be debited to income and expenditure account. Any profit on sale of fixed assets. Shown on credit side of income and expenditure a/c.

(iv) Sale of old periodicals

- The-receipt out of sale of newspaper and periodicals should be shown oh debit side of receipt and payment a/c

- Sale of newspaper and periodicals is the revenue, it should be transfer to income and expenditure a/c credit side as income.

(v) Sale of sports materials – Sale of sports materials dr items are’ capital receipts. The accounting treatment is as treatment of sale of fixed assets. Sports materials is a part of fixed assets.

(vi) Life membership fee:

- The person normally paid fees to the organization foe the intention to become life member of the organization. It is the revenue of the organization, shown an debit side of receipt and payment a/c.

- Life membership fees is the capital receipt in its nature. These fees amount are added to the capital fund on the liability side of the balance sheet.

![]()

Question 6.

Show the treatment of items of Income and Expenditure Account when there is a specific fund for those items.

Answer:

Specific fund or special donational are received by the non-profit organisations for specific reasons.

These receipts are capital receipts. Example of such funds are donations, Government funds/ grands.

The specific fund is normally a Capital Receipts any Payment out of such fund should reduced from balance sheet and normally any expenditures related to such fund should be debited to Income and Expenditure Accounts.

Special fund kept aside for special event and such fund should be in balance sheet liability side and reduction or any reduction should be reduced in balance sheet through the Income and Expenditure.

Question 7.

What is Receipts and Payments Account? How is it different from Income and Expenditure Account?

Answer:

Receipts and payments account is the summary of cash and bank transactions which helps in the preparation of income and expenditure account arid the balance sheet.

| Receipts and payments A/c | Income and expenditure A/c |

| (i) It is a real account. | (i) It is a nominal account. |

| (ii) It is prepared from the cash book. | (ii) It is prepared from the receipts and payments and other information. |

| (iii) It is on the basis of actuals Receipts and Payments and not considered accruals. | (iii) In this statement accruals of Receipts and Payments considered. |

| (iv) The different treated as cash balance or bank balance. | (iv) The different treated as profit or deficit for the year. |

2nd PUC Accountancy Accounting for Partnership : Basic Concepts Numerical Questions and Answers

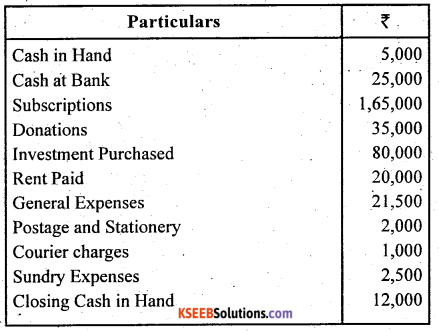

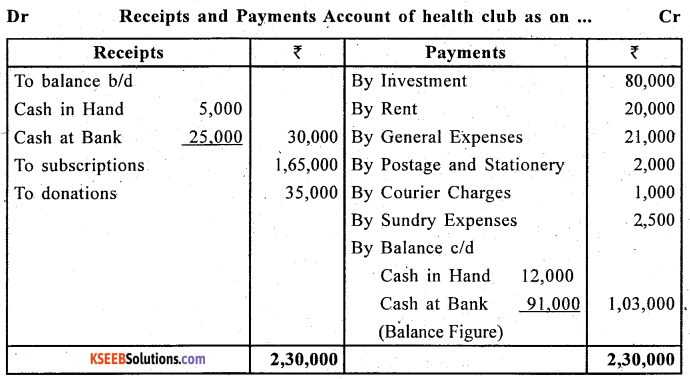

Question 1.

From the following particulars taken from the Cash Book of a health club, prepare a Receipts and Payments Account.

Answer:

![]()

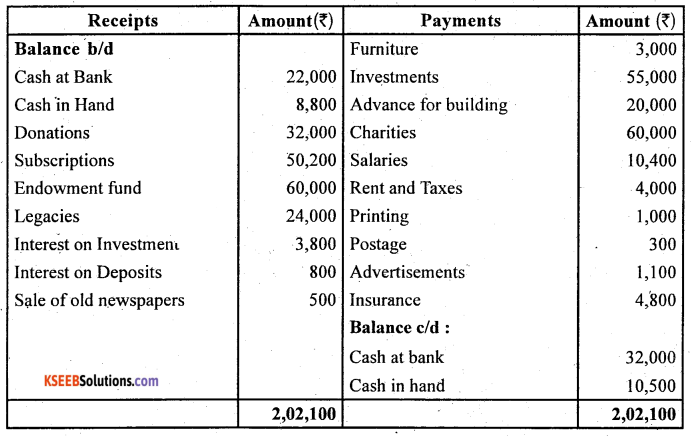

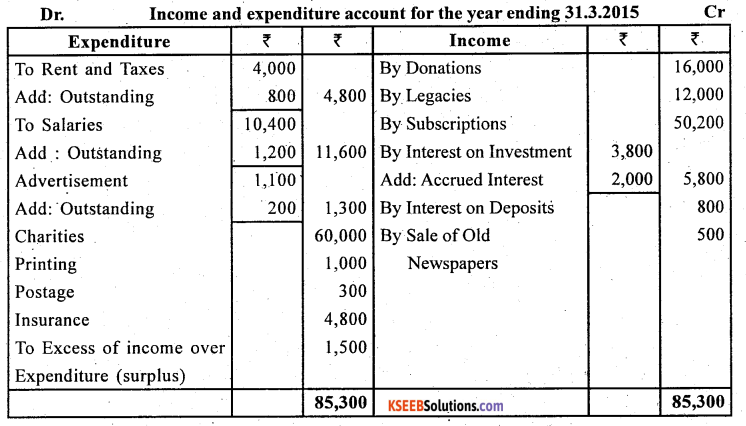

Question 2.

The Receipt and Payment Account of Harimohan Charitable Institution is given: Receipt and Payment Account for the year ending March 31, 2015

Answer:

Prepare the Income and Expenditure Account for the Year ended on March 31, 2015 after considering the following:

(i) It was decided to treat 50%.of the amount received on account of Legacies and Donations as Income.

(ii) Liabilities to be provided for are:

Rent₹ 800; Salaries ₹ 1,200; advertisement ₹ 200.

(iii) ₹ 2,000 due for interest on Investment was not actually received.

Solution:

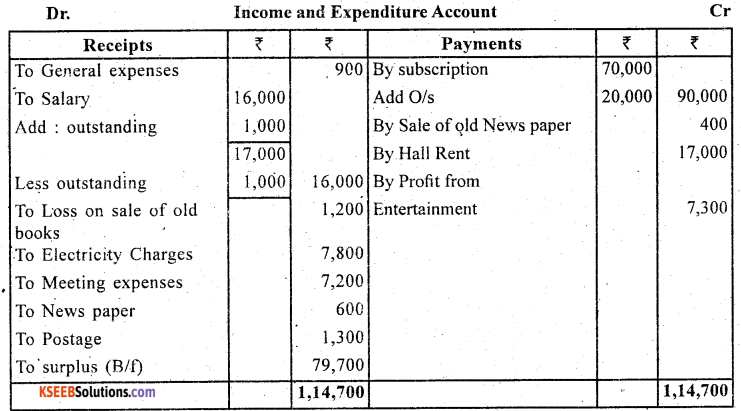

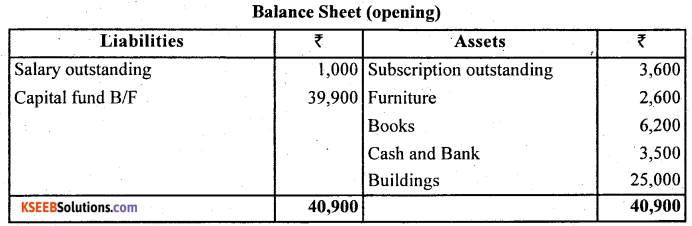

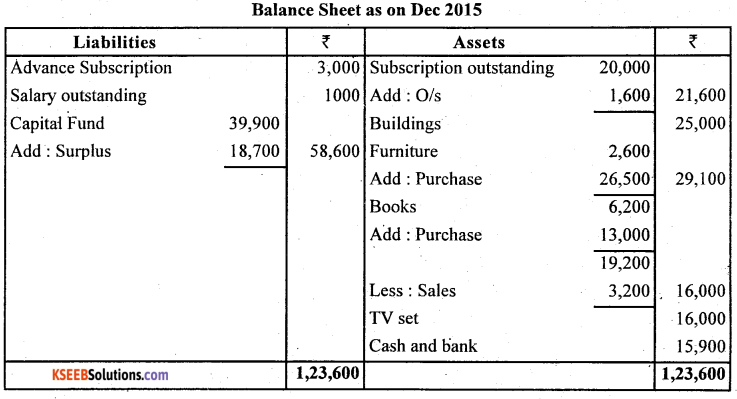

Question 3.

From the following particulars, prepare Income and Expenditure account:

Solution:

Question 4.

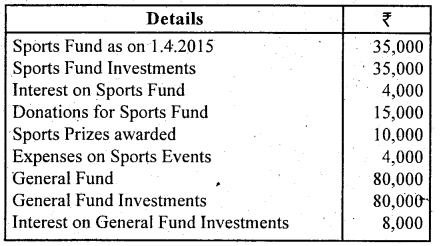

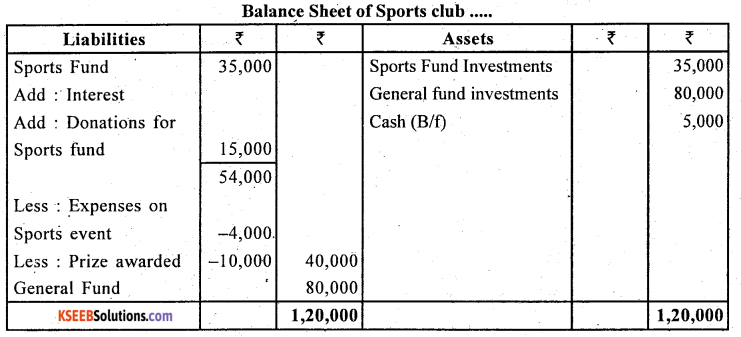

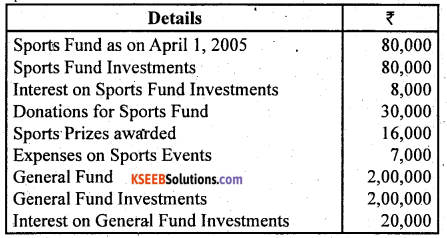

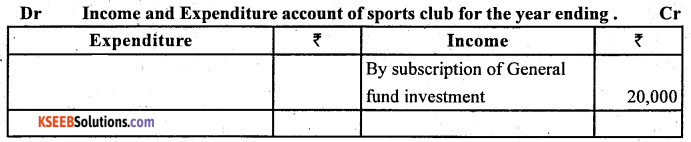

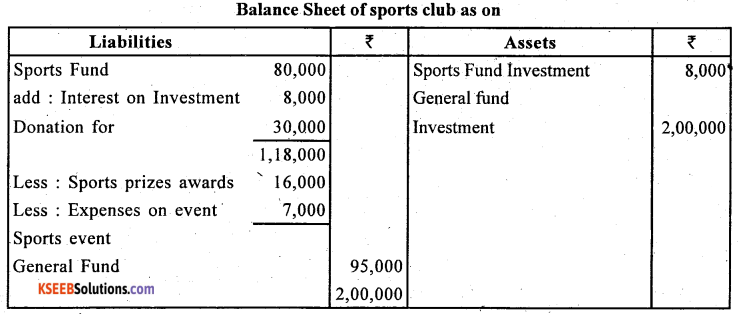

Following is the information given in respect of certain items of a Sports Club. Show these items in the Income and Expenditure Account and the Balance Sheet of the Club:

Solution:

Income and expenditure account of Sports Club for the year ending 31.3.2016

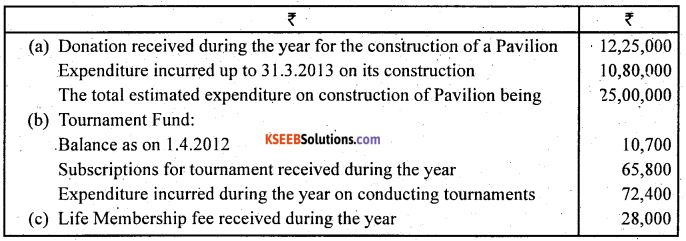

Question 5.

How will you deal with, the following items while preparing for the Bombay Women Cricket Club, its Income and Expenditure account for the year ending 31.3.2013 and its Balance Sheet as on 31.3.2013:

Give reasons for your answer.

Solution:

(a) Balance Sheet of Bombay Women Cricket Club as a March 31, 2013

(b)

(c)

![]()

Question 6.

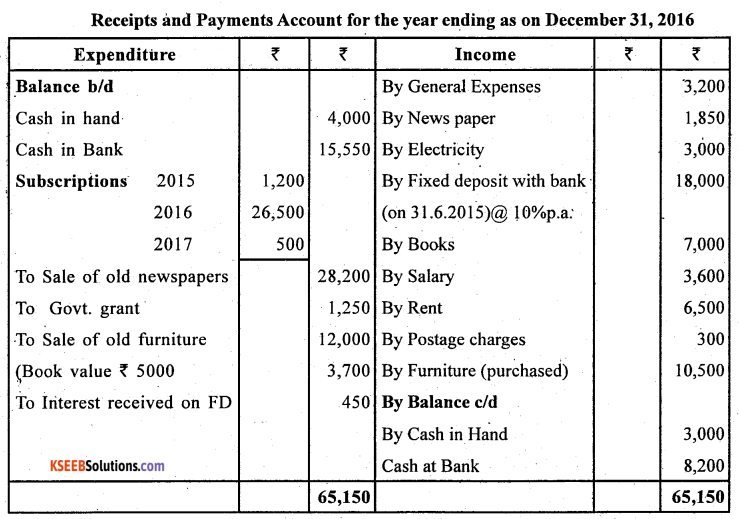

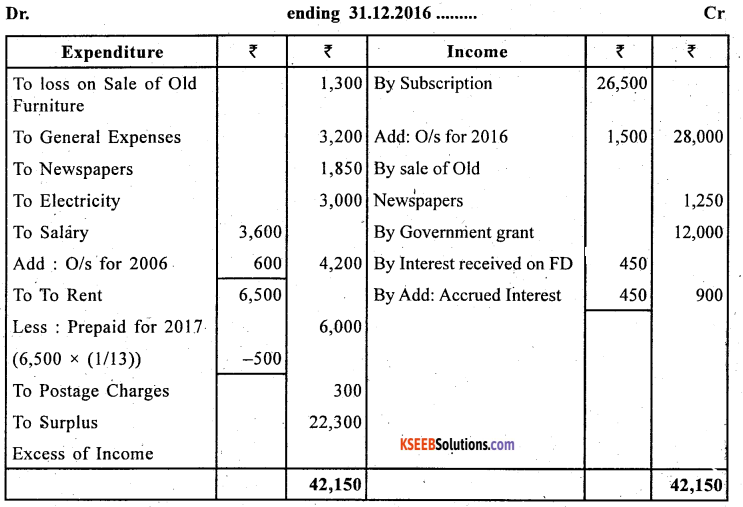

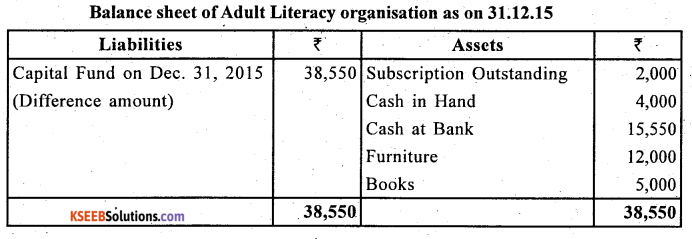

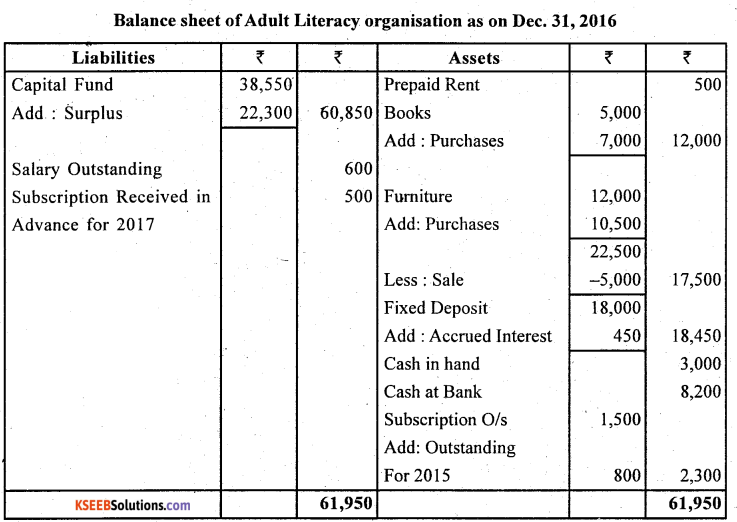

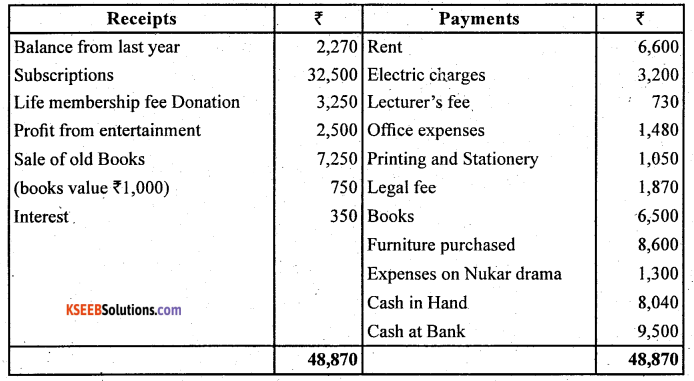

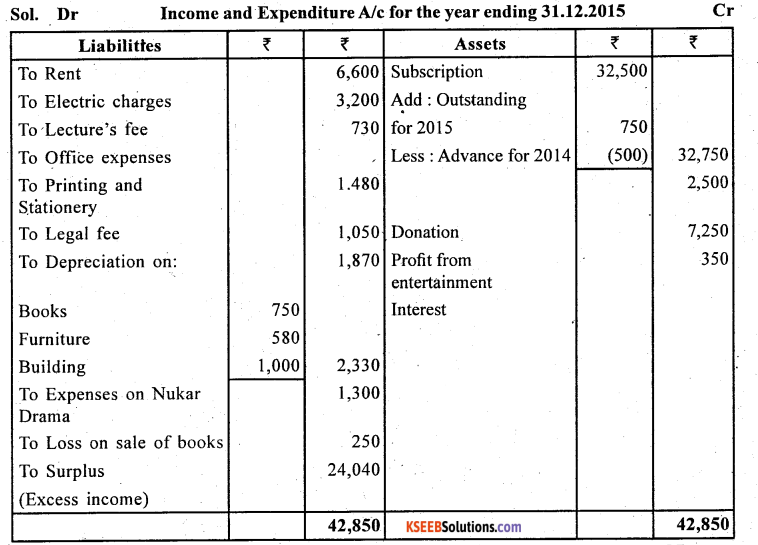

From the following Receipts and Payments and information given below, Prepare Income and Expenditure Account and opening Balance Sheet of Adult Literacy Orgnisation as on December 31,2016,

Information:

(i) Subscription outstanding as on 31.12.2015 ₹ 2,000 and on December 31, 2016 ₹ 1,500.

(ii) On December 31, 2016 Salary outstanding ₹ 600, and one month Rent paid in advance,

(iii) On Jan. 01,2015 orgnisation owned Furniture ₹ 12,000, Books ₹ 5,000.

Solution:

Income and Expenditure account of Adult Literacy Organisation for the year

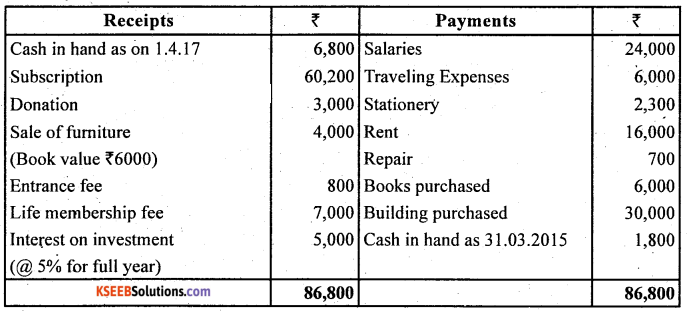

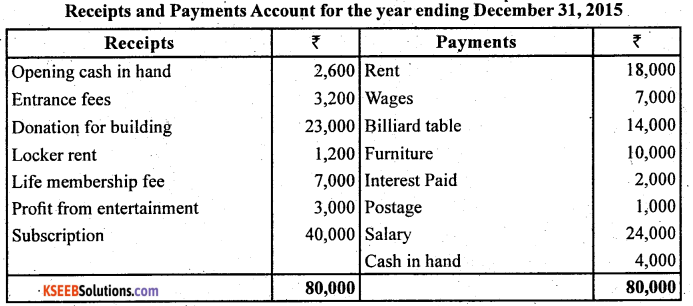

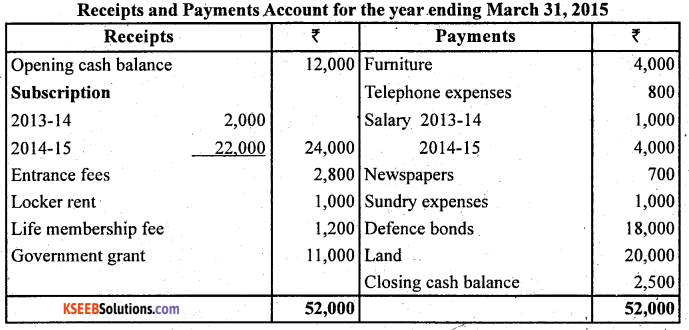

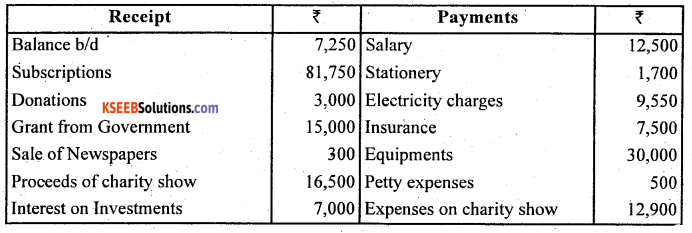

Question 7.

The following is the account of cash transactions of the Nari Kalayan Samittee for the year ended December 31, 2015:

You are required to prepare an Income and Expenditure Account after the following adjustments:

(a) Subscription still to be received is ₹ 750 , but subscription include ₹ 500 for the year 2014.

(b) In the beginning of the year the Sangh owned building ₹ 20,000 and furniture ₹ 3,000 and Books ₹ 2,000.

(c) Provide depreciation on furniture @5% (including purchase ), books @ 10% and building @ 5%.

Solution:

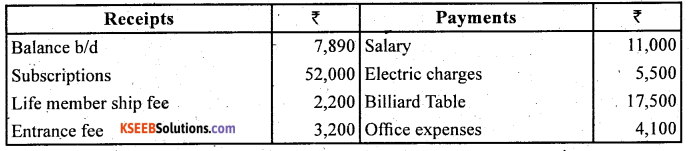

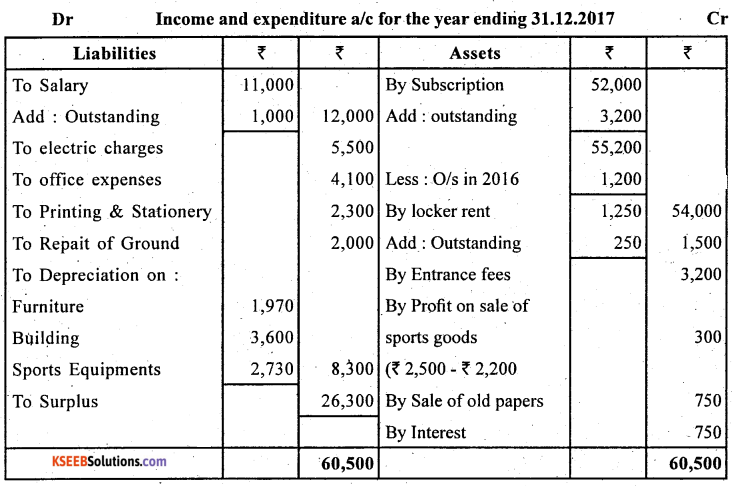

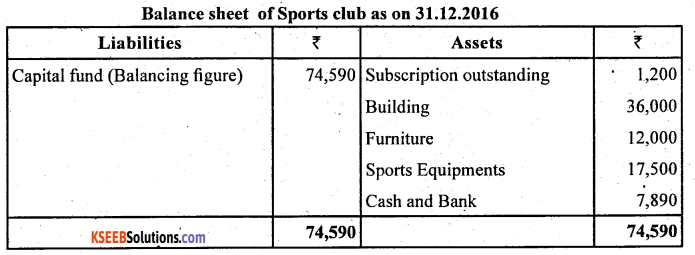

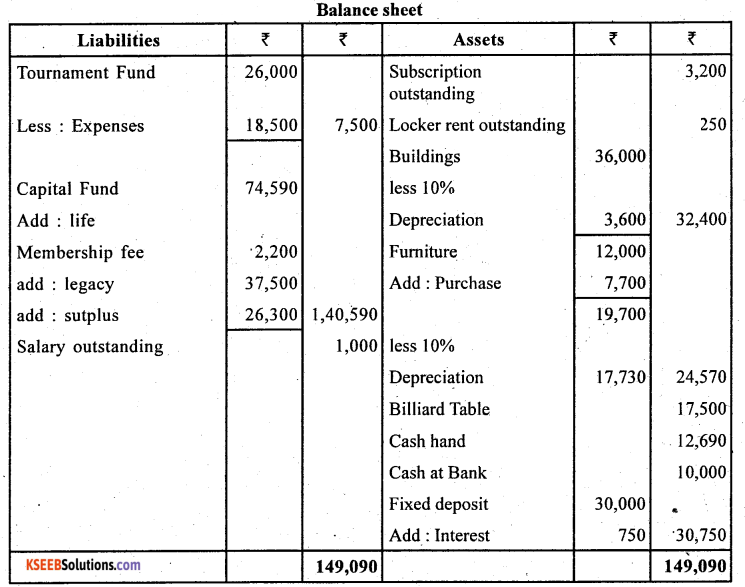

Question 8.

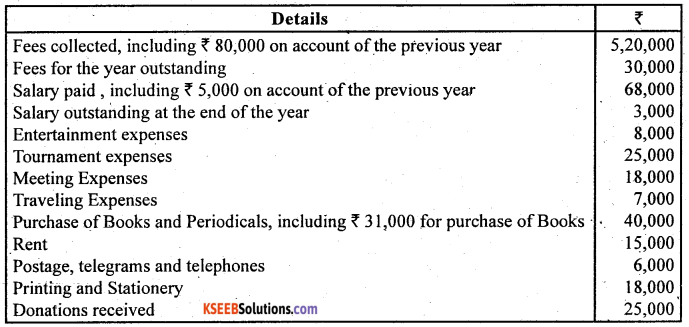

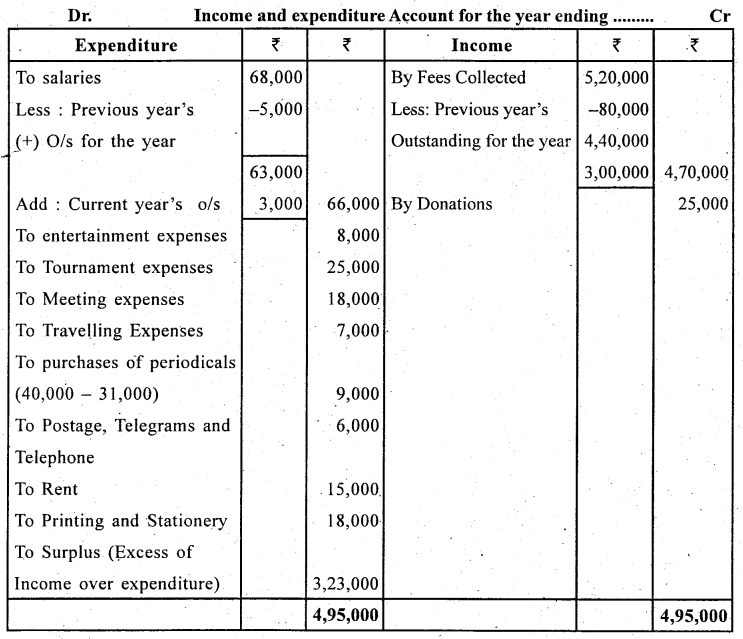

Following is the Receipt and Payment Account of Indian Sports Club, prepared Income and Expenditure Account, Balance Sheet as on December 31, 2017:

Receipts and Payments Account for the year ending December 31, 2017

Other Information:

Subscription outstanding was on December 31, 2016, ₹ 1,200 and ₹ 3,200 on December 31, 2017. Locker rent outstanding on December 31, 2018 ₹ 250. Salary outstanding on December 31,2017 ₹ 1,000.

On January 1,2017, club has Building ₹ 36,000, furniture ₹ 12,000, Sports equipments ₹ 17,500. Depreciation charged on these items @ 10% (including Purchase).

Solution:

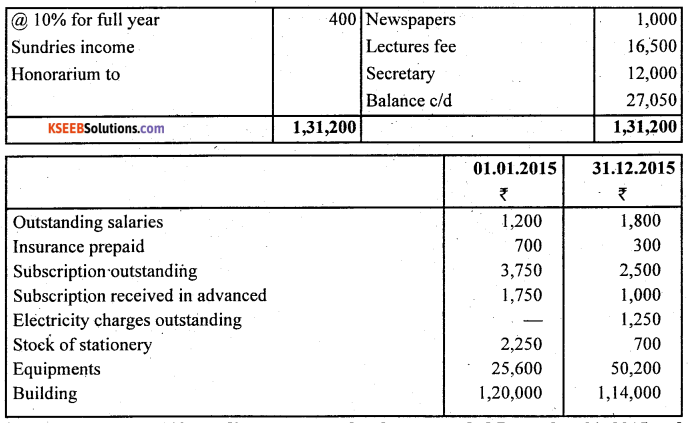

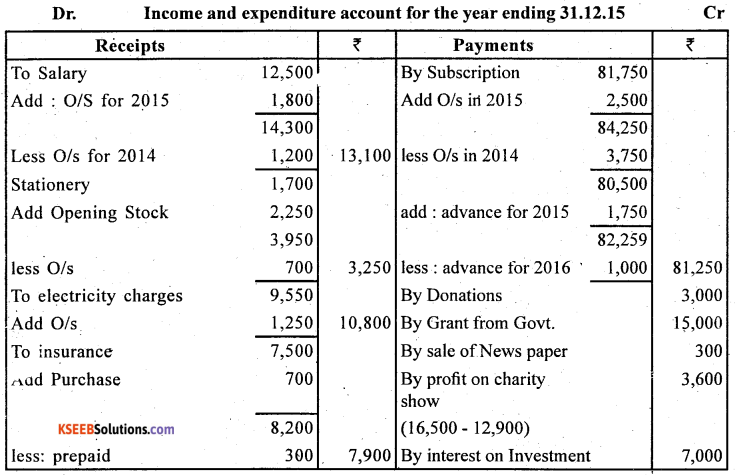

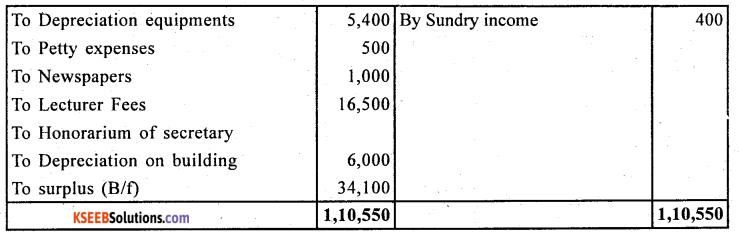

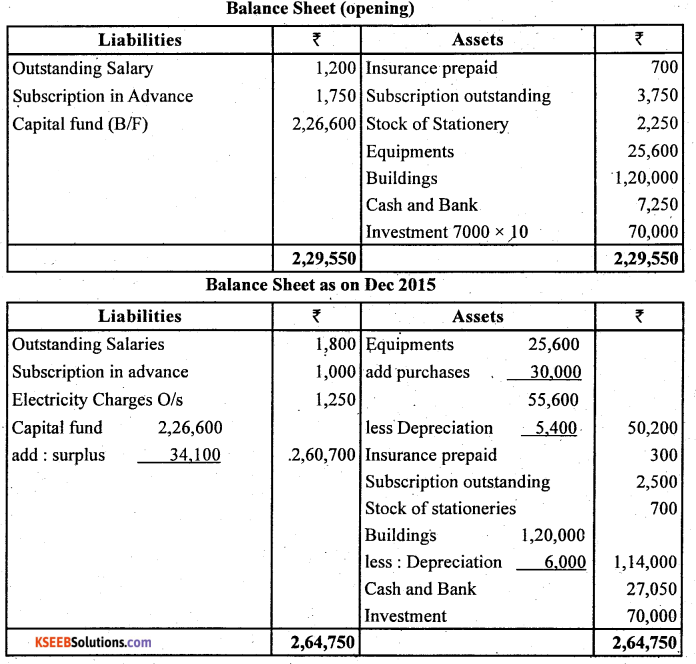

![]()

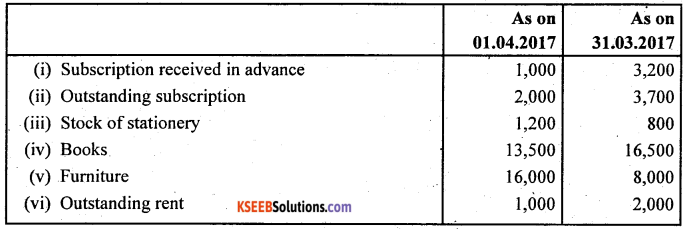

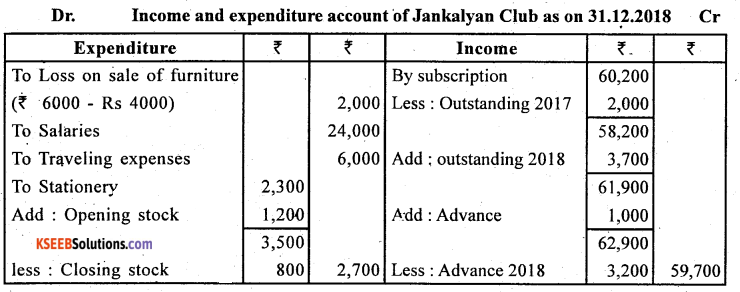

Question 9.

From the following Receipts and Payments Account of Jan Kalyan Club, prepare Income and Expenditure Account and Balance Sheet for the year ending March 31, 2018.

Receipt and Payment Account for the year ending March 31,2018

Additional Information:

Question 10.

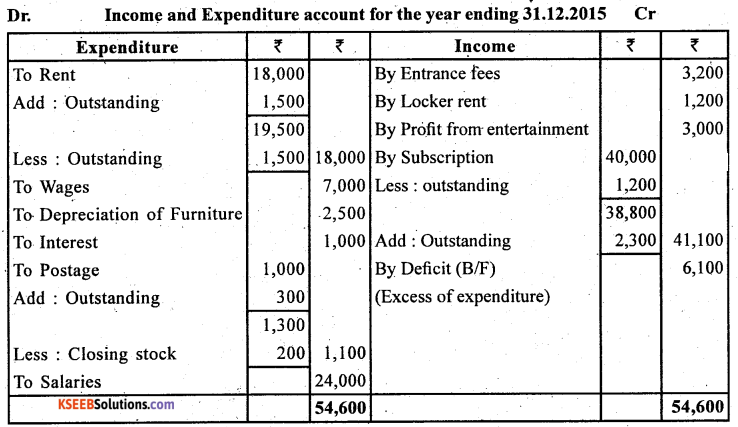

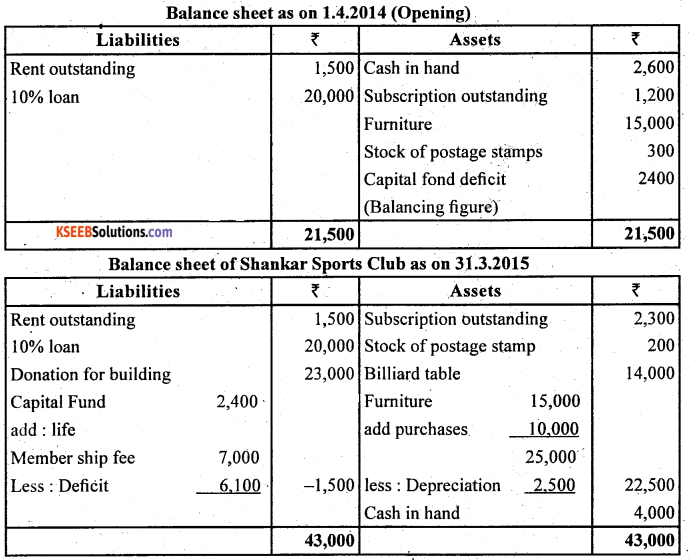

Receipts and Payments Account of Shankar Sports club is given below, for the year ended March 31,2015

Prepare Income and Expenditure Account and Balance Sheet with help of the following Information:

Subscription outstanding on March 31, 2014, is ₹ 1,200 and ₹ 2,300 on March 31, 2015, opening stock of postage stamps is ₹ 300 and closing stock is ₹ 200, Rent ₹ 1,500 related to 2005 and ₹ 1, 500 is still unpaid.

On April 1,2014 the club owned furniture ₹ 15,000, Furniture valued at ₹ 22,500 On March 31,2015. The club took a loan of ₹ 20,000 (@ 10% p.a) in 2014.

Question 11.

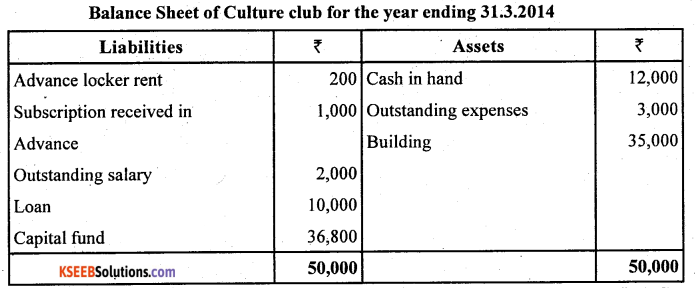

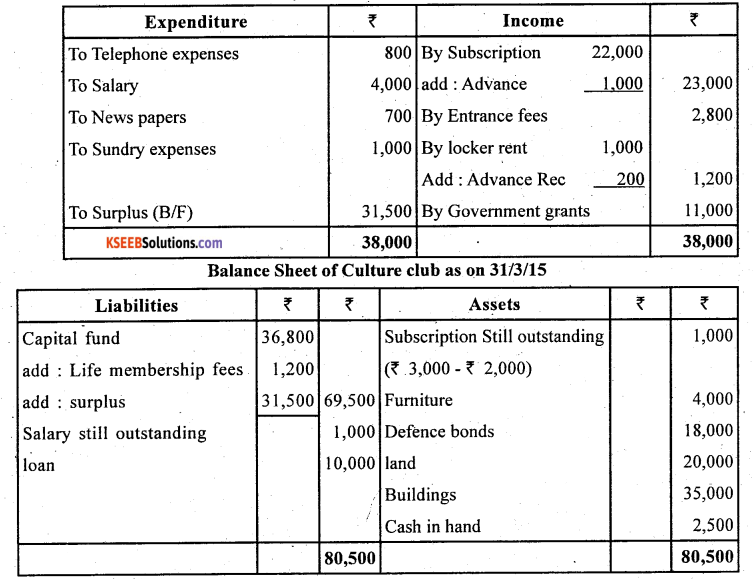

Prepare Income and Expenditure Account and Balance Sheet for the year ended March 31, 2015 from the following Receipts and Payment Account and Balance Sheet of culture club:

Solution :

![]()

Question 12.

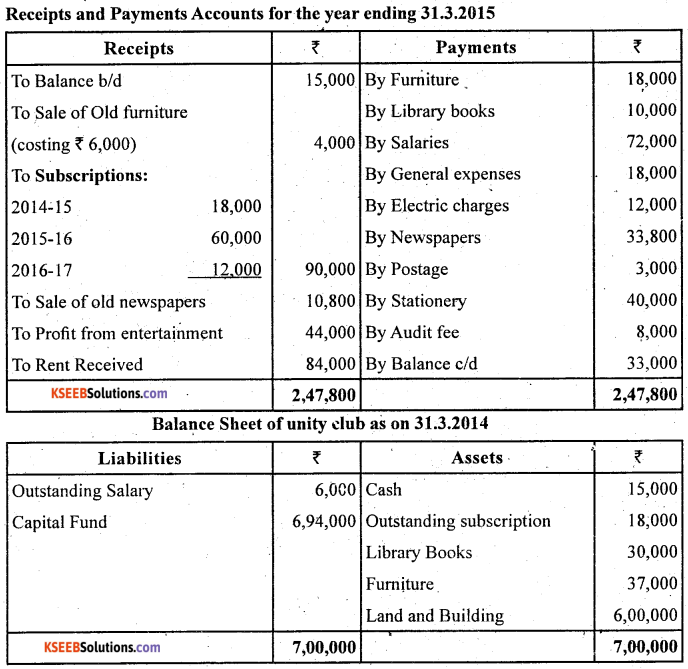

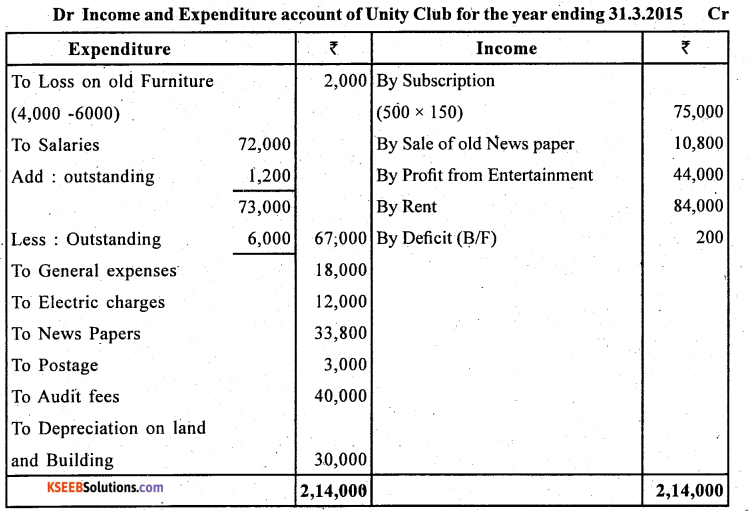

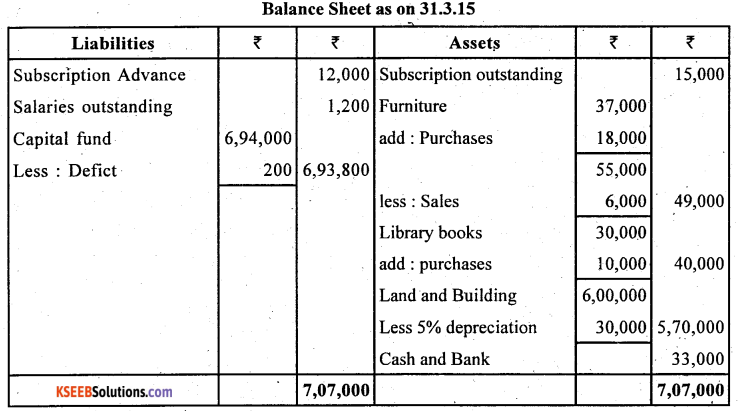

From the following Receipt and Payment Account prepare final accounts of a Unity Club for the year ended March 31, 2015.

Additional Information:.

1. The Club had 500 members each paying an annual subscription of ₹ 150.

2. On 31.3.2015 salaries outstanding amounted to ₹ 1,200 and salaries paid included ₹ 6,000 for the year 2013-14.

3. Provide 5% depreciation on Land and Building.

Question 13.

Following is the information in respect of certain items of a Sports Club. You are required to show them in the Income and Expenditure Account and the Balance Sheet.

Solution:

Note : Balance sheet wall not tally since information available is not sufficient.

![]()

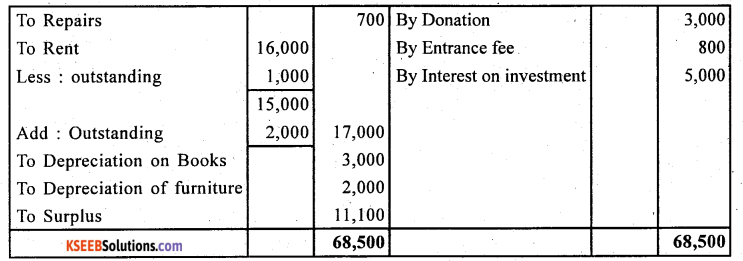

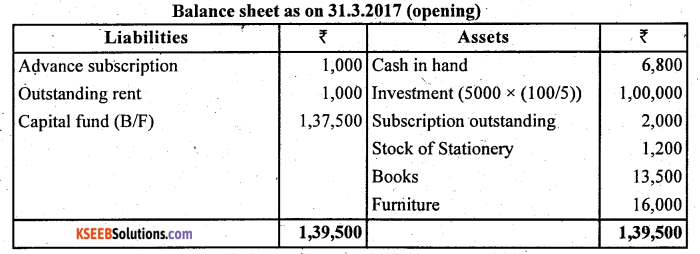

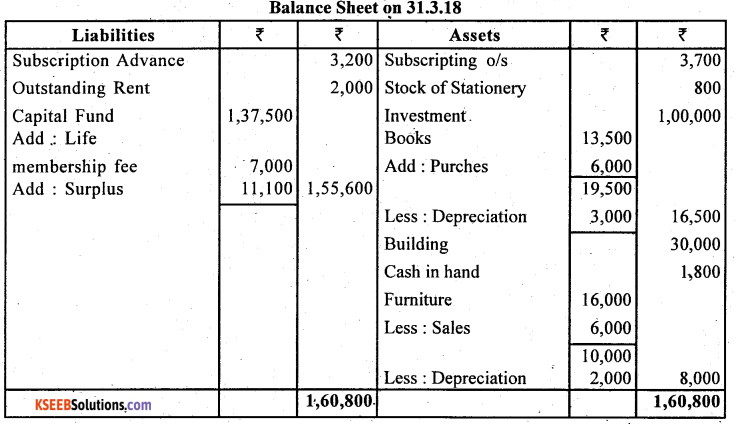

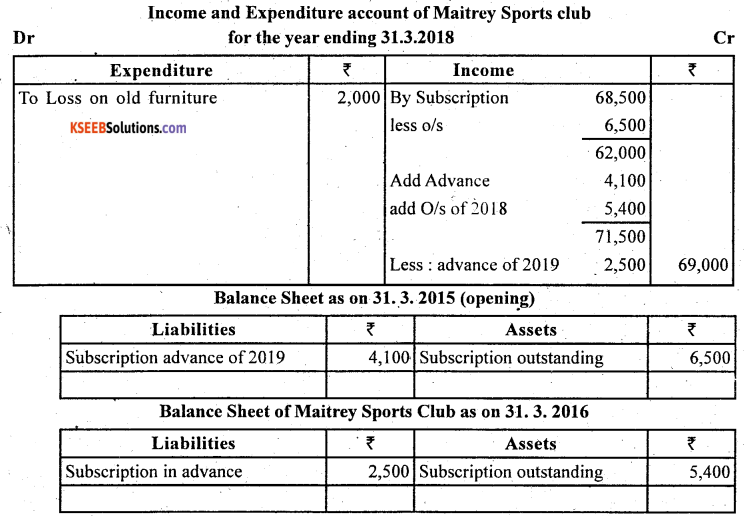

Question 14.

Receipt and Payment Account of Maitrey Sports Club showed that ? 68,500 were received by way of subscriptions for the year ended on March 31,2016.

The additional information was as under:

1. Subscription Outstanding as on March 31,2015 were ₹ 6,500,

2. Subscription received in advance as on March 31,2015 were ₹ 4,100,

3. Subscription Outstanding as on March 31,2016 were ₹ 5,400,

4. Subscription received in advance as on March 31,2016 were ₹ 2,500.

Show how that above information would appear in the final accounts for the year ended on March 31,2018 of Maitrey Sports Club.

Solution:

Question 15.

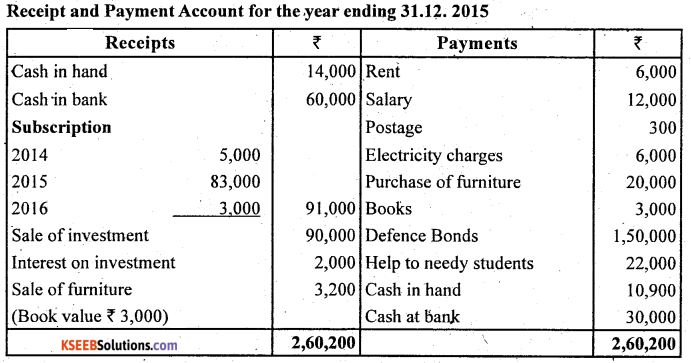

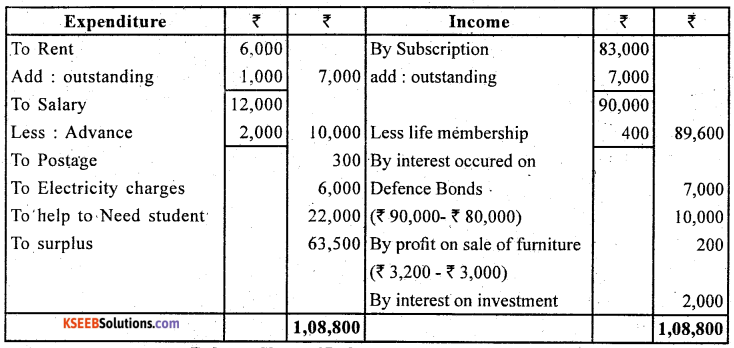

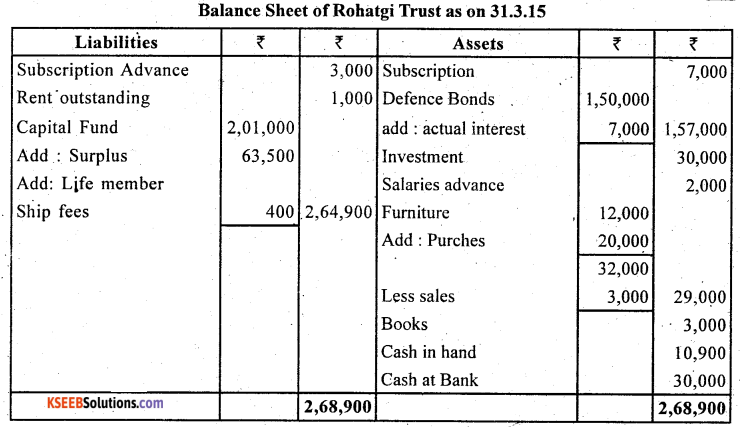

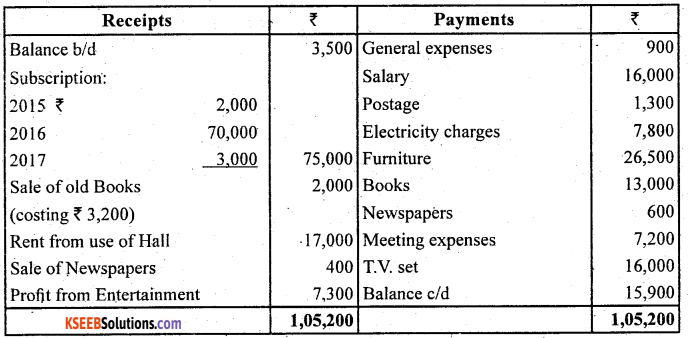

Following is the Receipt and Payment account of Rohatgi Trust:

Prepare Income and expenditure account for the year ended December 31,2015, and a Balance sheet as on that date after the following adjustments: –

Subscription for 2015, still owing were ₹ 7,000. Interest due on defence bonds was ₹ 7,000, Rent still owing was ₹ 1,000. The Book value of investment sold was ₹ 80,000, ₹ 30,000 of the investment were still in hand. Subscription received in 2015 included ₹ 400 from a life member. The total Furniture on January 1, 2015 was worth ₹ 12,000. Salary paid for the year 2014 is ₹ 2, 000.

Solution:

Dr. Income and expenditure account of Rohatgi Trust for the year ending 31.12.2015 Cr

Question 16.

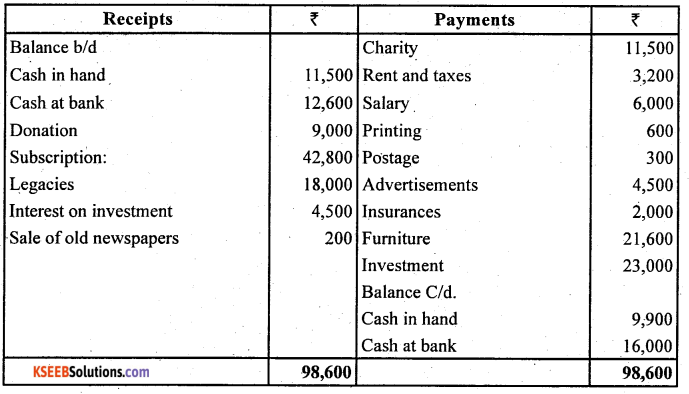

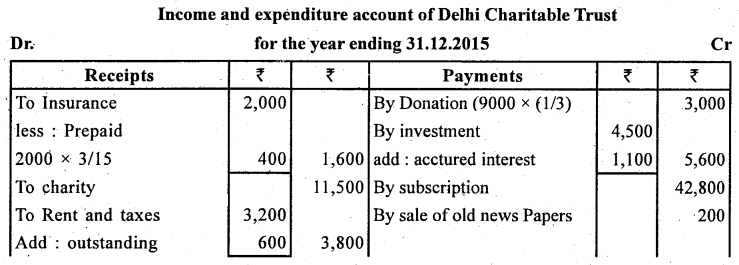

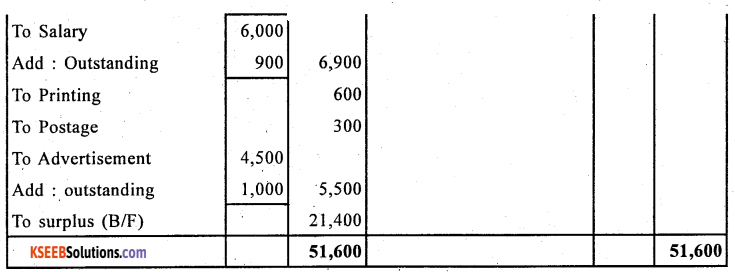

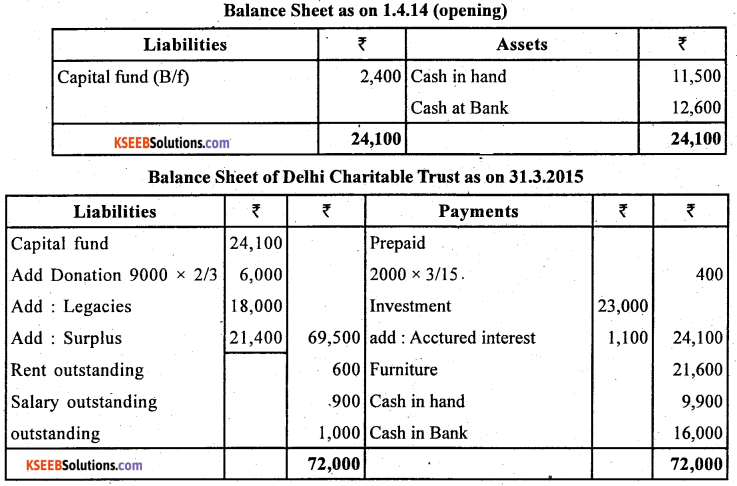

Following Receipt and Payment Account was prepared from the cash book of Delhi Charitable Trust for the year ending December 31, 2007

Receipts and Payments Account for the year ending December 31, 2007

Prepare Income and expenditure account for the year ended December 31, 2014, and a balance sheet as on that date after the following adjustments:

(a) It was decided to treat one-third of the amount received on account of donation as income.

(b) Insurance premium was paid in advance for three months.

(c) Interest on investment ₹ 1,100 accrued was not received. ‘

(d) Rent ₹ 600: salary ₹ 900 and advertisement expenses ₹ 1,000 outstanding as on December 31, 2015.

Solution:

Question 17.

From the following Receipt and Payment Account of a club, prepare Income and Expenditure Account for the year ended December 31, 2016 and the Balance Sheet as on that date.

Receipts and Payments Account for the year ending December 31, 2016

Additional Information:

(a) The club has 100 members, each paying an annual subscription of ? 900. Subscriptions outstanding on December 31,2016 were ₹ 3,600.

(b) On December 31, 2016, Salary outstanding amounted to ₹ 1,000, Salary paid included ₹ 1,000 for the year 2015.

(c) On January 1, 2016 the club owned Land and Building ₹ 25,000, Furniture ₹ 2,600 and Books ₹ 6,200.

Solution:

![]()

Question 18.

Following is the Receipt and Payment Account of Women’s Welfare Club for the year ended December 31, 2015:

Receipt and Payment Account for the year ending December 31, 2015

Prepare Income and Expenditure Account for the year ended December 31, 2015 and Balance Sheet as on that date.

Solution:

Question 19.

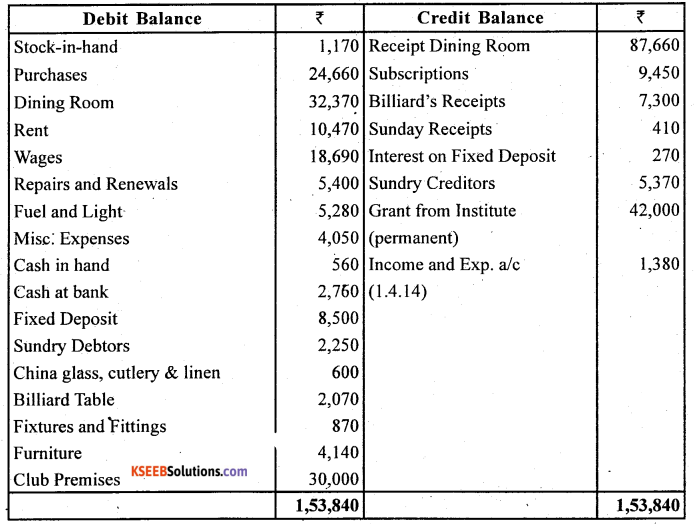

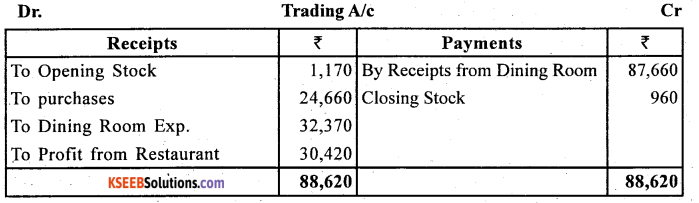

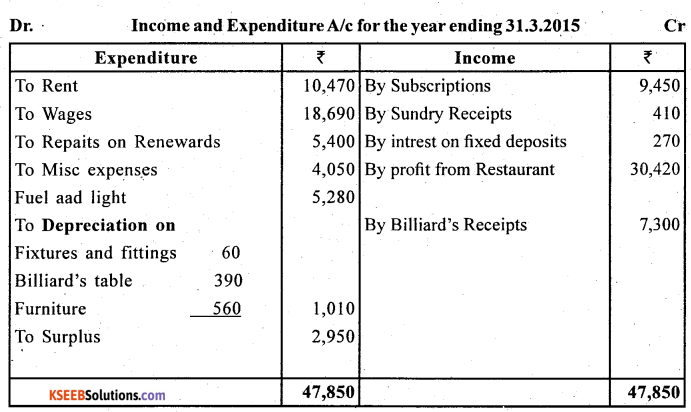

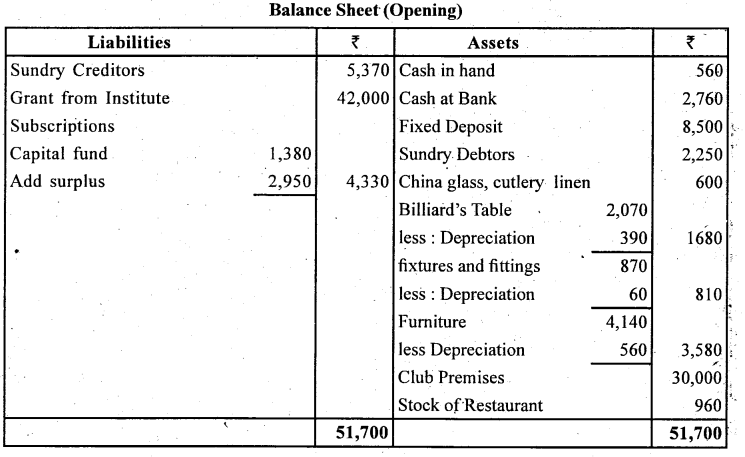

As at March 31, 2015 the following balance have been extrated from the books of the Indian Chartered Accountants Recreation Club and you are asked to prepare (1) Trading account for ascertaining gross profit derived from running restaurant and dining room and (2) income and expenditure account for the year ended March 31, 2015 (3) and a balance sheet as at the date:

On March 32, 2015 stock of restaurant consisted of ₹ 900 and ₹ 60 respectively. Provide Depreciations ₹ 60 on Fixtures, ₹ 390 on Billiard table and ₹ 560 on Furniture.

![]()

Test your Understanding – I

State with reasons whether the following statements are TRUE or FALSE:

(i) Receipt and Payment Account is a summary of all capital receipts and payments.

Answer:

False

(ii) If there appears a sports fund, the expenses incurred on sports activities will be shown on the debit side of Income and Expenditure Account.

Answer:

False

(iii) A credit balance of Income and Expenditure Account denotes excess if expenses over incomes.

Answer:

False

(iv) Scholarships granted to students out of funds provided by government will be debited to Income and Expenditure Account.

Answer:

False

![]()

(v) Receipt and Payment Account records the receipts and payments of revenue nature only.

Answer:

False

(vi) Donations for specific purposes are always capitalized.

Answer:

True

(vii) Opening balance sheet is prepared when the opening balance, of capital fund is not given.

Answer:

True

(viii) Surplus of Income and Expenditure Account is deducted from the capital/ general fund.

Answer:

True

(ix) Receipt and Payment Account is equivalent to profit and loss account. .

Answer:

False

(x) Receipt and Payment Account does not deference between capital and revenue receipts.

Answer:

True

![]()