You can Download Chapter 5 Dissolution of Partnership Firm Questions and Answers, Notes, 2nd PUC Accountancy Question Bank with Answers Karnataka State Board Solutions help you to revise complete Syllabus and score more marks in your examinations.

Karnataka 2nd PUC Accountancy Question Bank Chapter 5 Dissolution of Partnership Firm

2nd PUC Accountancy Dissolution of Partnership Firm NCERT Textbook Questions and Answers

2nd PUC Dissolution of Partnership Firm Short Answer Questions With Answers

Question 1.

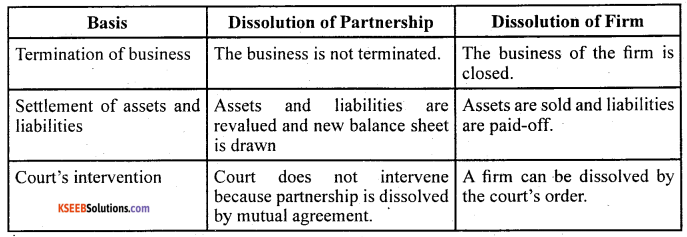

State the difference between dissolution of partnership and dissolution of partnership firm.

Answer:

Question 2.

State the accounting treatment for:

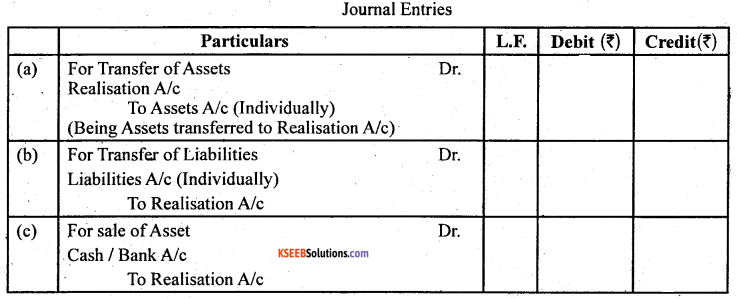

1. Unrecorded assets

2. Unrecorded liabilities

Answer:

For realisation of any unrecorded assets including goodwill, if any

Bank A/c Dr.

To Realisation A/c

10. For settlement of any unrecorded liability Realisation A/c Dr.

To Bank A/c

![]()

Question 3.

On dissolution, how will you deal with partner’s loan if it appears on the

(a) assets side of the balance sheet,

(b) liabilities side of balance sheet.

Answer:

Treatment partners loan: While writing entry related to loan, we have to b serve that loan paid by the partner, then firm liable to repay. At the time of dissolution the loan amount should be transferred to partners capital a/c credti side.

Incase of firm has paid has paid loan to partnership firm at appears in assets side of balance sheet. Such amount should be transferred t respective/concmed partners capital a/c debit side.

Question 4.

Distinguish between firm’s debts and partner’s private debts.

Answer:

Private Debts and Firm’s Debts: Where both the debts of the firm and private debts of a partner co-exist, the following rules, as stated in Section 49 of the Act, shall apply.

(a) The property of the firm shall be applied first in the payment of debts of the firm and then the surplus, if any, shall be divided among the partners as per their claims, which can be utilised for payment of their private liabilities.

(b) The private property of any partner shall be applied first in payment of his private debts and the surplus, if any, may be utilised for payment of the firm’s debts, in case the firm’s liabilities exceed the firm’s assets.

It may be noted that the private property of the partner does not include the personal properties of his wife and children. Thus, if the assets of the firm are not adequate enough to pay off firm’s liabilities, the partners have to contribute out of their net private assets

Question 5.

State the order of settlement of accounts on dissolution.

Answer:

Settlement of Accounts: In case of dissolution of a firm, the firm ceases to conduct business and has to settle its accounts. For this purpose, it disposes off all its assets for satisfying all the claims against it. In this context it should be noted that, subject to agreement among the partners, the following rules as provided in Section 48 of the

Partnership Act 1932 shall apply.

(a) Treatment of Losses

Losses, including deficiencies of capital, shall be paid:

- first out of profits,

- next out of capital of partners, and

- lastly, if necessary, by the partners individually in their profits sharing ratio.

Question 6.

On what account realisation account differs from revaluation account

Answer:

| Revalution a/c | Realisation |

| It is prepared at the time of admission retirement or death of a partner | It is prepared at the time of closure of business i.e dissolution |

| Revised only these assets and liability are revalued | All assets and external liabilities are record which are payable |

| Unrecorded assets liabilities will not be given much importance | All unrecorded assets and liabilities are recorded on respective side. |

2nd PUC Dissolution of Partnership Firm Long Answer Questions With Answers

Question .

What is meant by dissolution of partnership firm?

Answer:

Dissolution of a partnership firm may take place without the intervention of court or by the order of a court, in any of the ways specified later in this section.

It may be noted that dissolution of the firm necessarily brings in dissolution of the partnership. Dissolution of a firm takes place in any of the following ways:

1. Dissolution by Agreement: A firm is dissolved :

(a) with the consent of all the partners or

(b) in accordance with a contract between the partners.

2. Compulsory Dissolution: A firm is dissolved compulsorily in the following cases:

(a) when all the partners or all but one partner, become insolvent, rendering them incompetent to sign a contract;

(b) when the business of the firm becomes illegal; or

(c) when some event has taken place which makes it unlawful for the partners to carry on the business of the firm in partnership, e.g., when a partner who is a citizen of a countiy becomes an alien enemy because of the declaration of war with his countiy and India.

![]()

3. On the happening of certain contingencies: Subject to contract between the partners, a firm is dissolved :

(a) if constituted for a fixed term, by the expiry of that term;

(b) if constituted to carry out one or more ventures, by the completion thereof;

(c) by the death of a partner;

(d) by the adjudication of a partner as an insolvent.

4. Dissolution by Notice: In case of partnership at will, the firm may be dissolved if any one of the partners gives a notice in writing to the other partners, signifying his intention of seeking dissolution of the firm.

5. Dissolution by Court: At the suit of a partner, the court may order a partnership firm to be dissolved on any of the following grounds:

(a) when a partner becomes insane;

(b) when a partner becomes permanently incapable of performing his duties as a partner;

(c) when a partner is guilty of misconduct which is likely to adversely affect the business of the firm;

(d) when a partner persistently commits breach of partnership agreement;

(e) when a partner has transferred the whole of his interest in the firm to a third party;

(f) when the business of the firm cannot be carried on except at a loss; or

(g) when, on any ground, the court regards dissolution to be just and equitable.

Question 2.

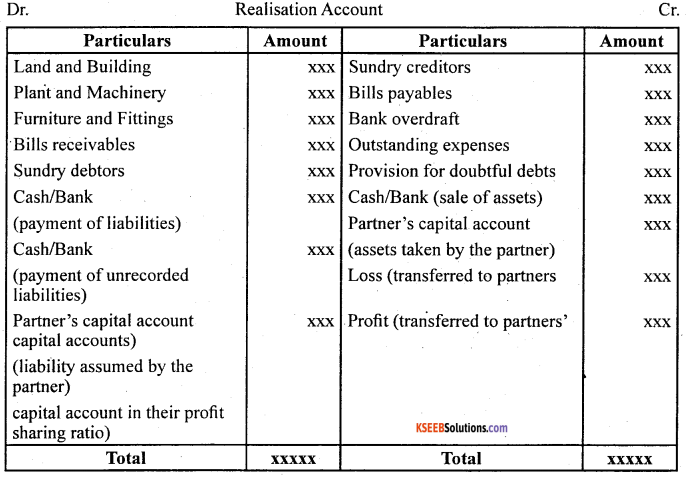

What is a Realisation Account?

Answer:

When the firm is dissolved, its books of account are to be closed and the profit or loss arising on realisation of its assets and discharge of liabilities is to be computed. For this purpose, a Realisation Account is prepared to ascertain the net effect (profit or loss) of realisation of ‘ assets and payment of liabilities which may be is transferred to partner’s capital accounts in their profit sharing ratio.

Hence, all assets (other than cash in hand bank balance and fictitious assets, if any), and all external liabilities are transferred to this account. It also records the sale of assets, and payment of liabilities and realisation expenses; The balance in this account is termed as profit or loss on realisation which is transferred to partners’ capital accounts in thier profit sharing ratio

Question 3.

Reproduce the format of Realisation Account.

Answer:

Question 4.

How deficiency of Crditors is paid off?

Answer:

For settlement with the creditor through transfer of assets when a creditor accepts an asset in full and final settlement of his account, journal entry needs to be recorded. But, if the creditor accepts an asset only as part payment of his/her dues, the entry will be made for cash payment only. For example, a creditor to whom ₹ 10,000 was due accepts office equipment worth ₹ 8,000 and is paid ₹ 2,000 in cash, the following entry shall be made for the payment of ₹ 2,000 only.

Realisation A/c Dr.

To Bank A/c

However, when a creditor accepts an asset whose value is more than the amount due to him, he/she will pay cash to the frim for the difference for which the entry will be:

BankA/c Dr.

To Realisation A/c

For payment of realisation expenses

(a) When some expenses are incurred and paid by the firm in the process of realisation of assets and payment of liabilities:

Realisation A/c Dr.

To Bank A/c

2nd PUC Dissolution of Partnership Firm Numerical Questions

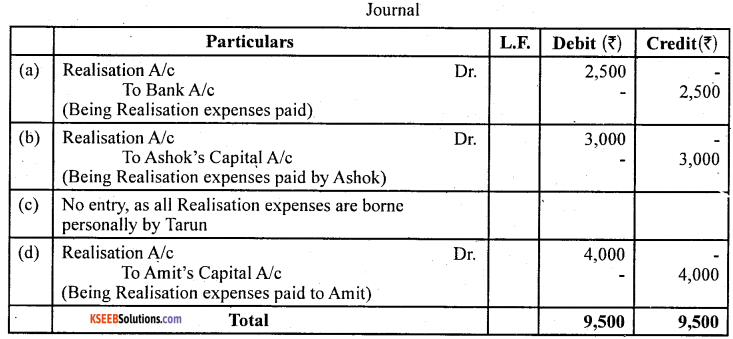

Question 1.

Journalise the following transactions regarding Realisation expenses:

(a) Realisation expenses amounted to ₹ 2,500.

(b) Reahisation expenses amounting to ₹ 3,000 were paid by Ashok, one of the partners.

(c) Realisation expenses ₹ 2,300 borne by Tarun, personally.

(d) Amit, a partner was appointed to realize the assets, at a cost of ? 4,000. Theactual amount of Realisation amounted to ₹ 3,000.

Answer:

![]()

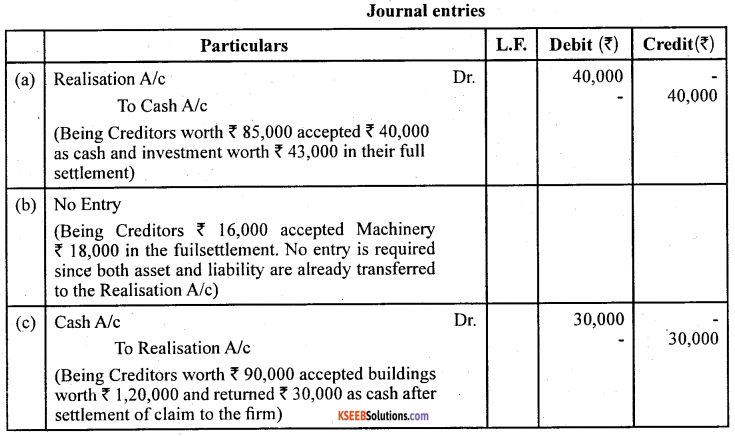

Question 2.

Record necessary journal entries in the following cases:

(a) Creditors worth ₹ 85,000 accepted ₹ 40,000 as cash and Investment worth ₹ 43,000, in full settlement of their claim.

(b) Creditors were ₹ 16,000. They accepted Machinery valued at ₹ 18,000 in settlement of their claim.

(c) Creditors were ₹ 90,000. They accepted Buildings valued ₹ 1,20,000 and paid cash to the firm ₹ 30,000.

Answer:

Question 3.

There was an old computer which was written-off in (the books of accounts in the pervious year. The same has been taken over by a partner Nitin for ₹ 3,000. Journalise the transaction, supposing. That the firm has been dissolved.

Answer:

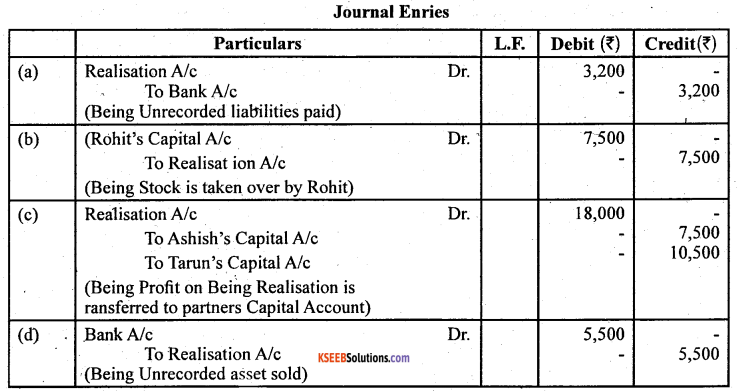

Question 4.

What journal entries will be recorded for the following transactions on the dissolution of a firm:

(a) Payment of unrecorded liabilities of ₹ 3,200.

(b) Stock worth ₹ 7,500 is taken by a partner Rohit.

(c) Profit on Realisation amounting to ₹ 18,000 is to be distributed between the partners Ashish and Tarun in the ratio of 5 : 7.

(d) An unrecorded asset realised ₹ 5,500.

Answer:

Question 5.

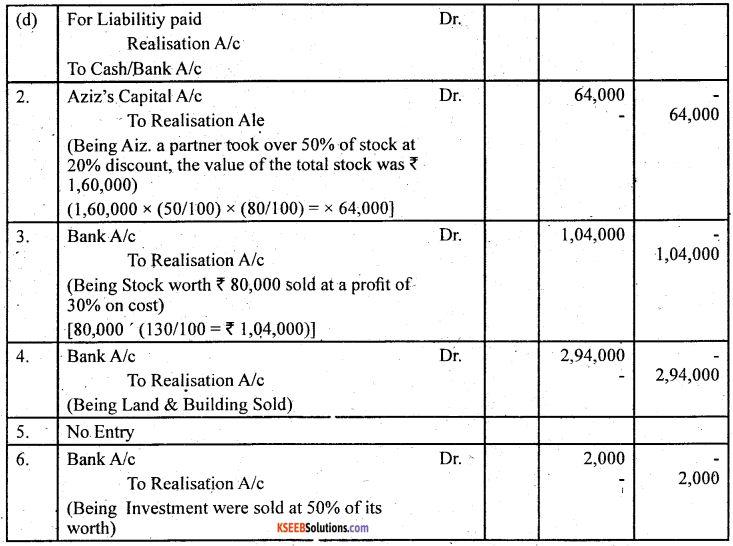

Give journal entries for the following transactions

1. To record the Realisation of various assets and liabilities.

2. A firm has a Stock of ₹ 1,60,000. Aziz, a partner took over 50% of the Stock at a of 29%

3. was sold at a profit of 30% on cost.

4. (book value ₹ 1,60,000) sold for ₹ 3,00,000 through a bro charged 2%, commission on the deal.

5. Plant and Machinery (book value ₹ 60,000) was handed over to a creditor at an agreed valuation of 10% less than the book value

6. Investment whose face value was ₹ 4,000 was realized at 50%

Answer:

![]()

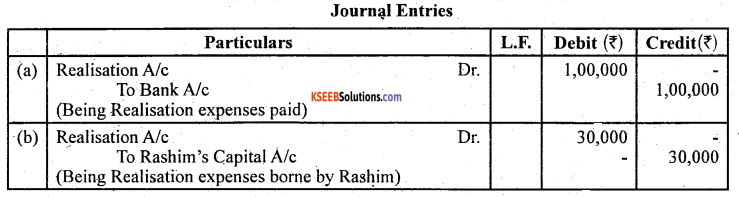

Question 6.

How will you deal with the realisation expenses of the firm of Rashim and Bindiya in the following cases:

1. Realisation expenses amounts to ₹ 1,00,000,

2. Realisation expenses amounts to ₹ 30,000 are paid by Rashini, a partner,

3. Realisation expenses are to be borne by Rashim for which he will be paid ₹ 70,000

as remuneration for completing the dissolution process. The actual expenses Incurred by Rashim were ₹ 1,20,000.

Answer:

Question 7.

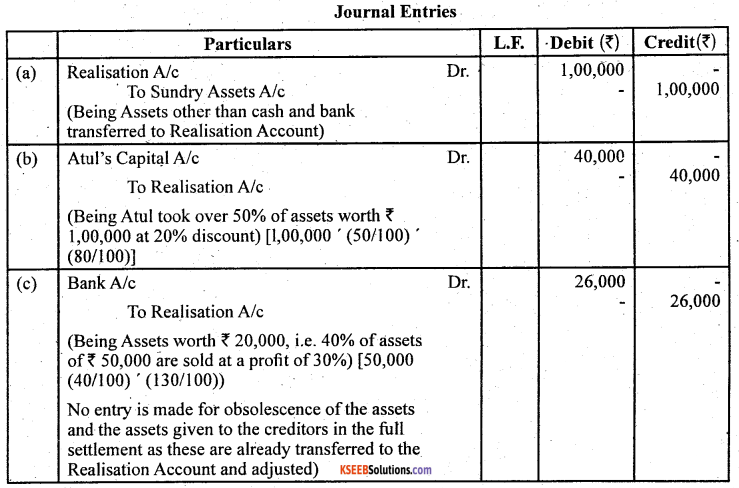

The book value of assets (other than cash and bank) transferred to Realisation Account is ₹ 1,00,000. 50% of the assets are taken over by a partner Atul, at a discount of 20%; 40% of the remaining assets are sold at a profit of 30% on cost; 5% of the balance being obsolete, realised nothing and remaining assets are handed over to a Creditor, in full settlement of his claim. You are required to record the journal entries for realisation of – assets.

Answer:

Question 8.

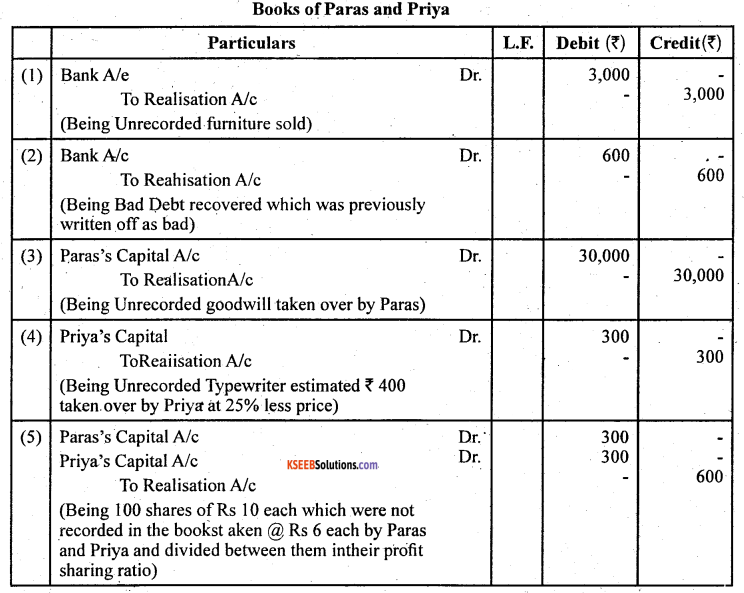

Record necessary journal entries to record the following Unrecorded assets ann liabilities in the books of Paras and Priya:

1. There was an old furniture in the firm which had been written-off completely in the books. This was sold for ₹ 3,000.

2. Ashish, an old customer whose account for ₹ 1,000 was written-off as bad in the previous year, paid 60%, of the amount.

3. Paras agreed to takeover the firm’s goodwill (not recorded in the books of the ‘ firm), at a valuation of ₹ 30,000,

4. There was aa old typewriter which had been written-off completely from the books. It was estimated to realize ₹ 400. It was taken away by Priya at an estimated price less 25%.

5. There were 100 shares of ₹ 10 each in Star Limited acquired at a cost of ₹ 2,000 which had been written-off completely from the books. These shares are valued ₹ 6 each and divided among the partners in their profit sharing ratio.

Answer:

Question 9.

All partners wishes to dissolve the firm. Yastin, a partner wants that her loan of ₹ 2,00,000 must be paid off before the payment of capitals to the partners. But, Amart, another partner wants that the capitals must be paid before the payment of Yastin’s loan. You are required to settle the conflict giving reasons.

Answer:

As per section 48 of Partnership Act 1932, at the time of dissolution, loans and advances from the partners must be paid off before the settlement of their capital accounts. Hence, Yastin’s argument is correct that her loan of ₹ 2,00,000 must be paid off before the payment of partners capital.

![]()

Question 10.

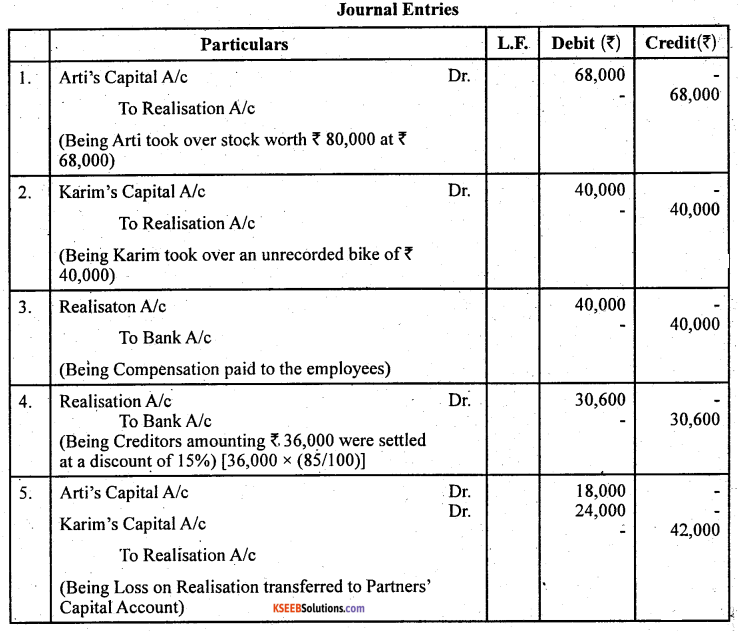

What journal entries would be recorded for the following transactions on the dissolution of a firm after various assets (other than cash) on the third party liabilities have been transferred to Realisation account

1. Arti took over the Stock worth ₹ 80,000 at ₹ 68,000.

2. There was unrecorded Bike of ₹ 40,000 which was taken over By Mr. Karim.

3. The firm paid ₹ 40,000 as compensation to employees. ,

4. Sundry creditors amounting to ₹ 36,000 were settled at a discount of 15%.

5. Loss on realisation ₹ 42,000 was to be distributed between Arti and Karim in the ratio of 3:4.

Answer:

Question 11.

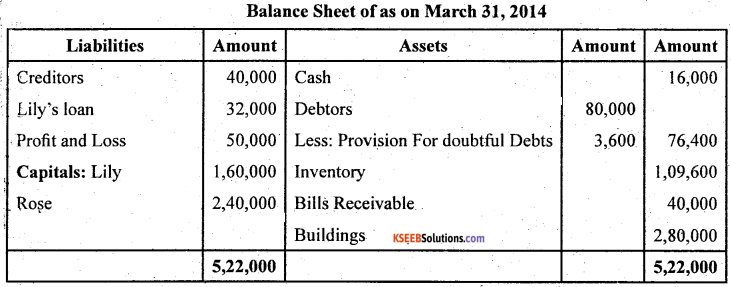

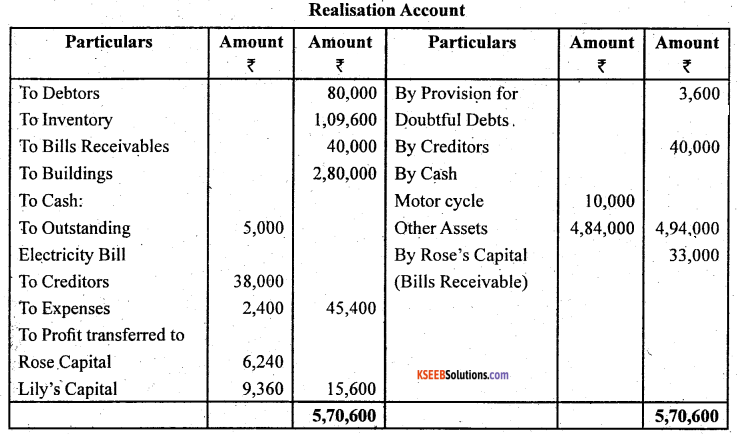

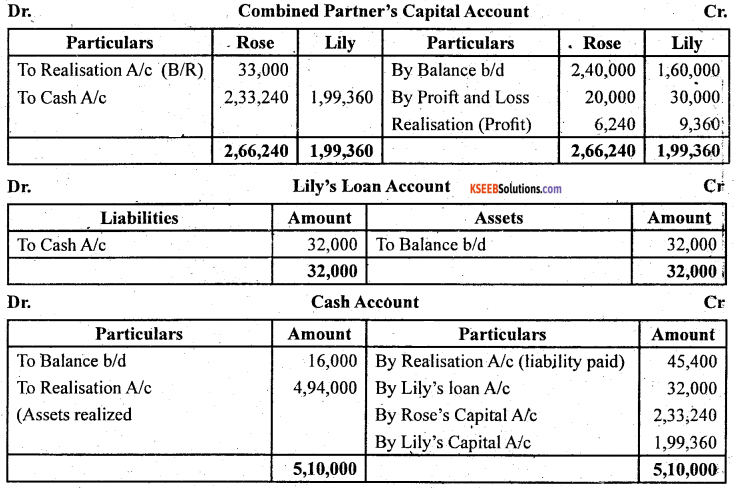

Rose and Lily shared profits in the ratio of 2 : 3. Their Balance Sheet 2014 was as follows:

Rose and. Lily decided to dissolve the firm on the above date. Assets except bills receivables) realised ₹ 4,84,000. Bills Receivable were taken over by Rose at ₹ 30,000. Creditors agreed to take ₹ 38,000. Cost of Realisation was ₹ 2,400. There was a Motor Cycle in the firm which was bought out of the firm’s money, was not shown in the books of the firm. It was now sold for ₹ 10,000. There was a contingent liability in respect of outstanding electric bill of ₹ 5,000, Bill Receivable taken over by Rose at ₹ 33,000.

Answer:

![]()

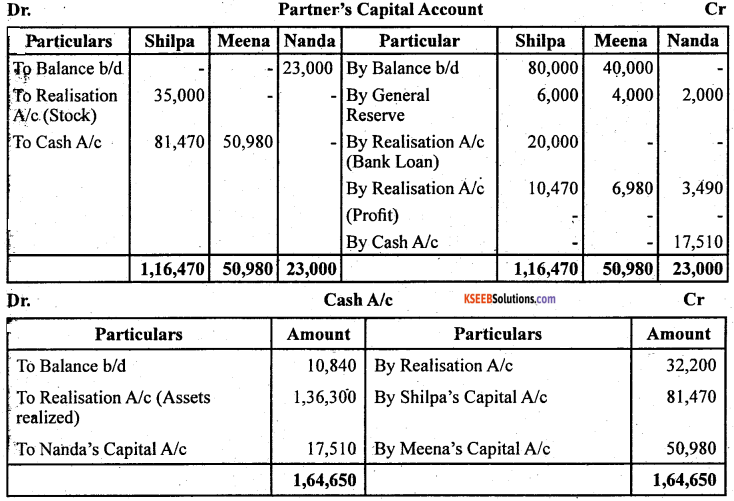

Question 12.

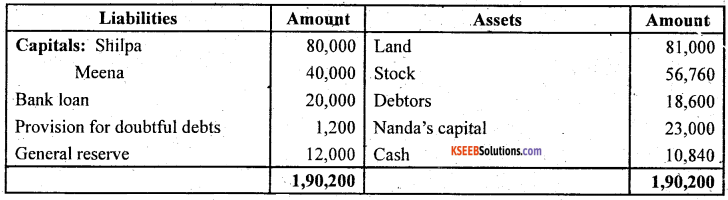

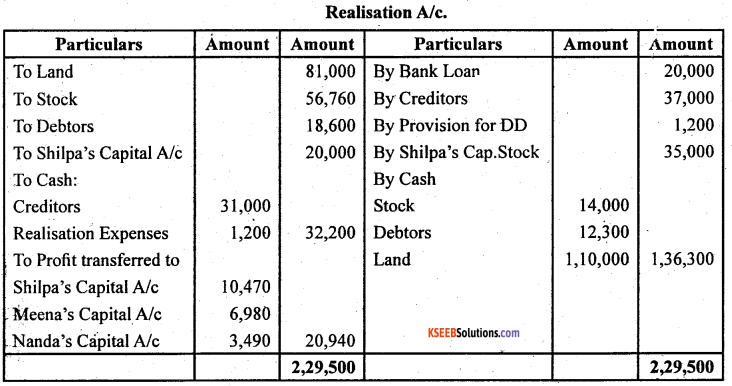

Shilpa, Meena and Nanda decided to dissolve their partnership oh March 31, 2014. Their profit, sharing ratio was 3:2:1 and their Balance Sheet was as under:

The stock of value of ₹ 41,660 are taken over by Shilpa for ₹ 35,000 and she agreed to discharge bank loan. The remaining stock was sold at ₹14,000 and debtors amounting toRs, 10,000 realised ₹ 8,000, land is sold for ₹ 1,10,000. The remaining debtors realized 50% at their book value. Cost of realization amounted to ₹ 1,200. There was a typewriter not recorded in the books worth ₹ 6,000 which were taken over by one of the Creditor at this value. Prepare Realisation A/c.

Answer:

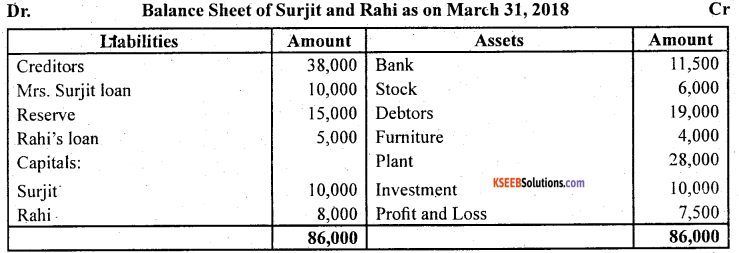

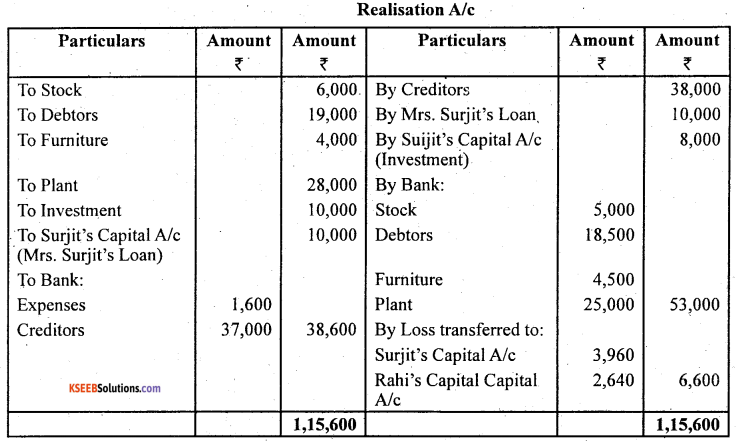

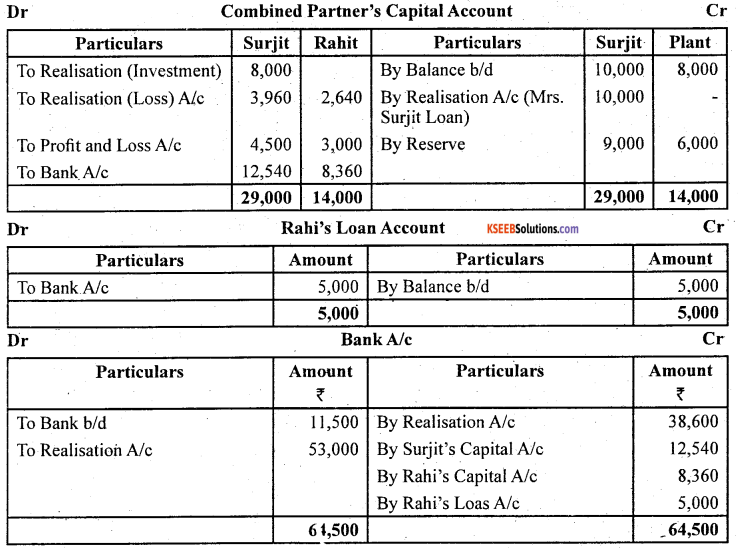

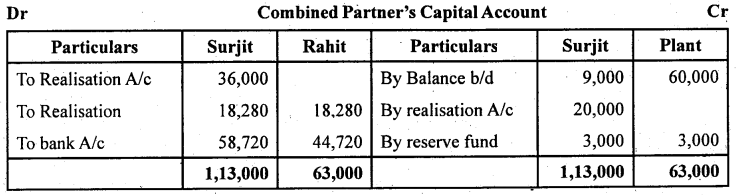

Question 13.

Surjit and Rahi were sharing profits (losses) in the ratio of 3:2, their Balance Sheet as on March 31, 2014 is as follows:

The firm was dissolved on March 31, 2014 on the following terms:

1. Surjit agreed to take the investments at ₹ 8,000 and to pay Mrs. Surojit’s loan.

2. Other assets were realised as follows: Stock ₹ 5,000, Debtors ₹ 18,500, Furniture ₹ 4,500, Plant ₹ 25,000

3. Expenses on realisation amounted to ₹ 1,600.

4. Creditors agreed to accept ₹ 37,000 as a final settlement.

You are required to prepare Realisation account, Partner’s Capital account and Bank account.

Answer:

![]()

Question 14.

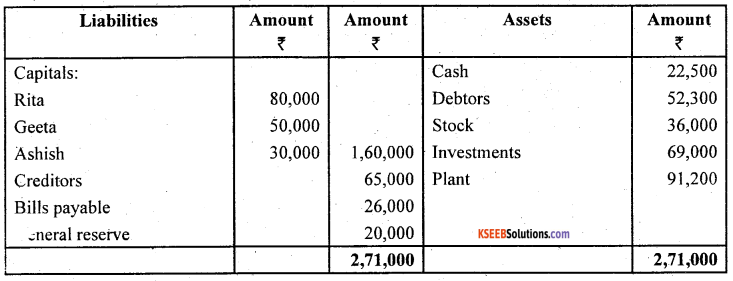

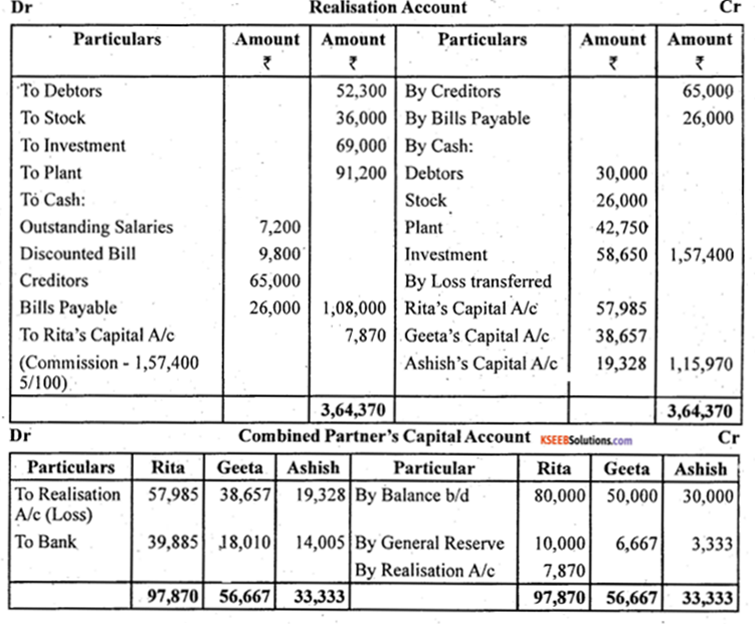

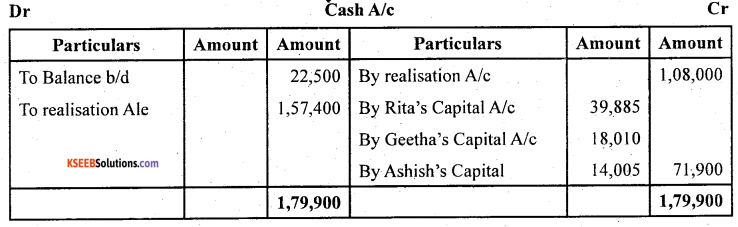

Rita, Geeta and Ashish were partners in a firm sharing profits/losses in the ratio of 3:2:1. On March 31,2014 their balance sheet was as follows:

On the date of above mentioned date the firm was dissolved:

1. Rita was appointed to realise the assets. Rita was to receive 5% commission on the rate of assets (except cash) and was to bear all expenses of realisation,

2. Assets were realised as follows:

Debtors 30,000

Stock 26,000

Plant 42,750

3. Investments were realised at 85% of the book value,

4. Expenses of realisation amounted to ₹ 4,100,

5. Firm had to pay ₹ 7,200 for outstanding salary not provided for earlier,

6. Contingent liability in respect of bills discounted with the bank was also materialized and paid off ₹ 9,800,’Prepare Realisation account, Capital Accounts of Partner’s and Cash Account.

Answer:

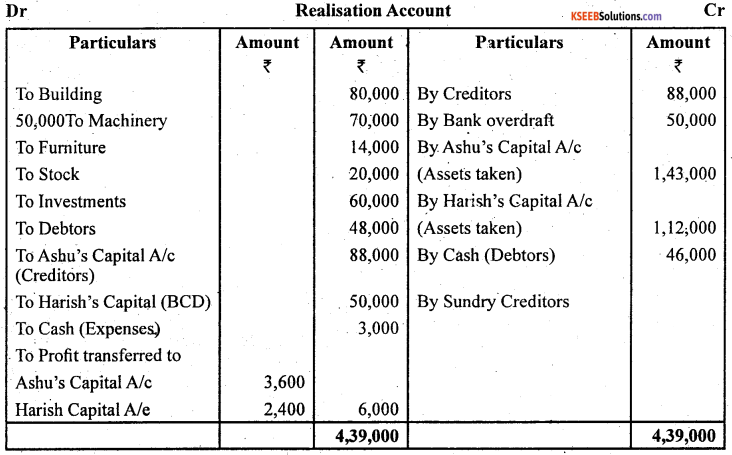

Question 15.

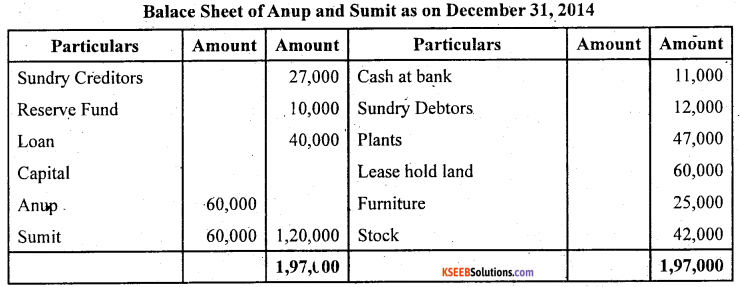

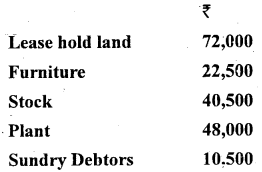

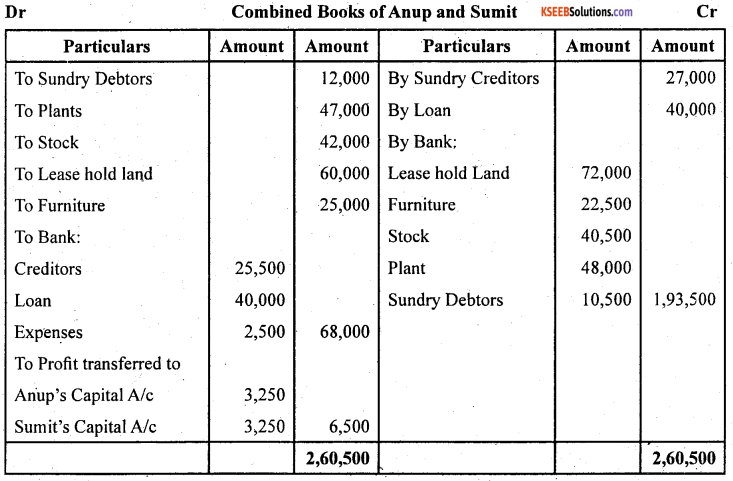

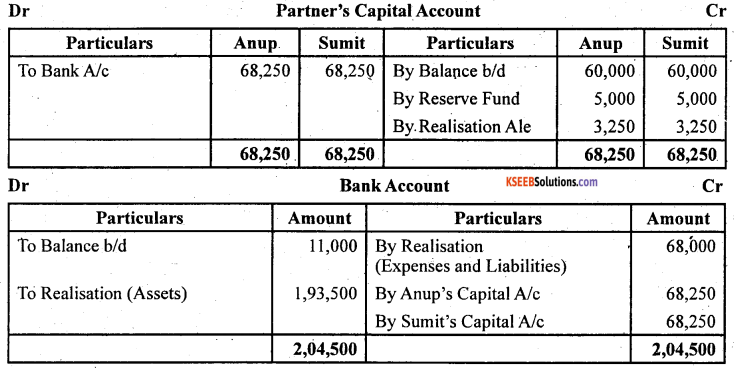

Anup and Suntit are equal partners in a firm. They decided to dissolve the parutership on December 31, 2014. When the balance sheet is as under

The Assets were realised as follows:

The Creditors were paid ₹ 25,500 in full settlement. Expenses of Realisation amount to ₹ 2,500.

Prepare Realisation Account, Bank Account, Partners Capital Accounts to close the books of the firm.

Answer:

![]()

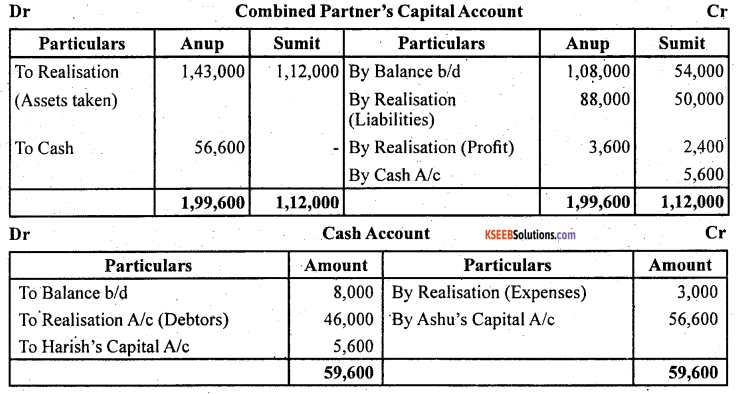

Question 16.

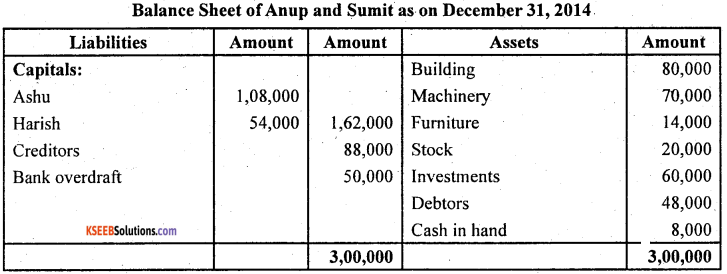

Ashu and Harish are partners sharing profit and losses as 3:2. They decided to dissolve the firm on December 31. 2014. Their balance sheet oil the above date was:

Asha is to take over the building at ₹ 95,000 and Machinery and Furniture is take over by Harish at value of ₹ 80,000. Ashu agreed to pay Creditor and Harish agreed to meet Bank overdraft. Stock and Investments are taken by both partner in profit sharing ratio. Debtors realised for ₹ 46,000, expenses of realisation amounted to ₹ 3,000: Prepare necessary ledger account.

Answer:

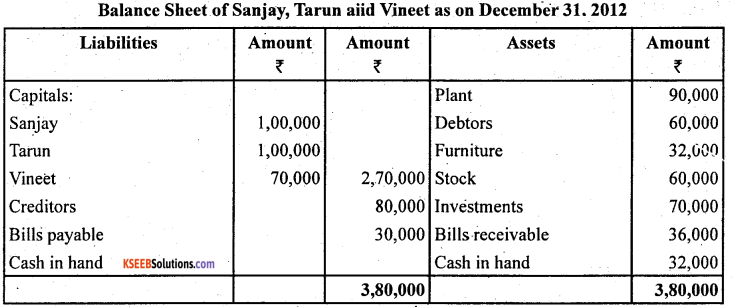

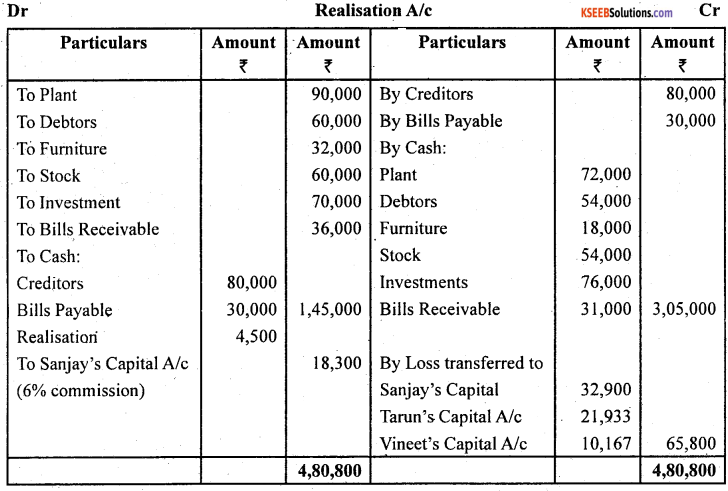

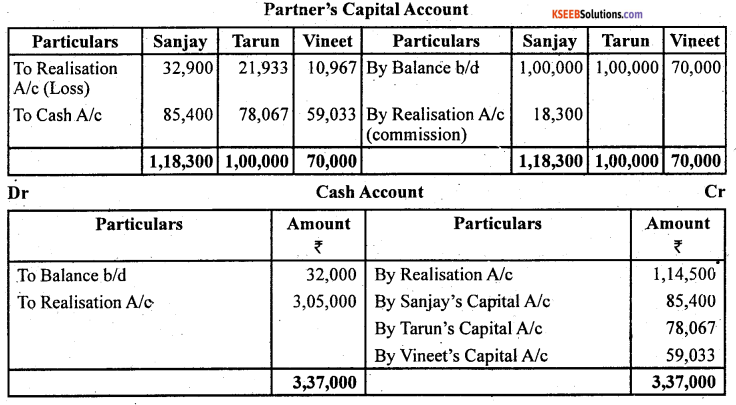

Question 17.

Sanjay, Tarun and Vineet shared profit in the ratio of 3:2:1. On December 31,2012 their balance sheet was as follows

On this date the firm was dissolved. Sanjay was appointed to realise the assets. Sanjay was to receive 6% commission on sale of assets (except cash) and was to bear all expenses of realisation. Sanjay realised the assets as follows: Plant ₹ 72,000, Debtors ₹ 4,000, Furniture ₹ 18,000, Stock 90% of the book value, Investments ₹ 76,000 and Bills receivable ₹ 31,000, Expenses of realisation amounted to ₹ 4,500. Prepare Realisation Account, Capital Accounts and Cash Account

Answer:

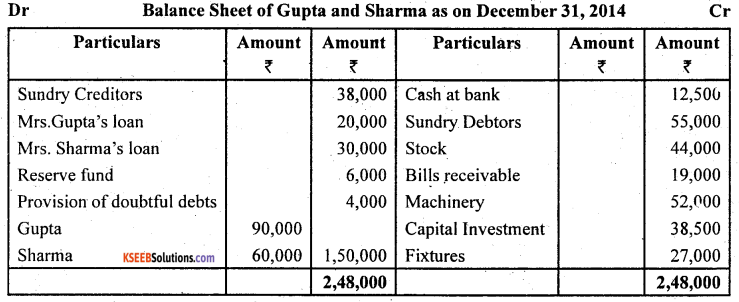

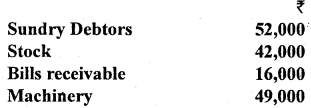

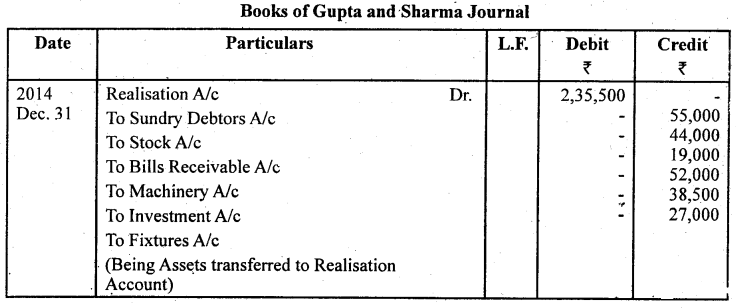

Question 18.

The following is the Balance Sheet of Gupta and Sharma as on December.

The firm was dissolved on December 31, 2014 and asset realised and settlements of liabilities as follows:

(a) The realisation of the assets were:

(b) Investment was taken over by Gupta at agreed value of ₹ 36,000 and agreed to pay of Mrs. Gupta’s loan.

(c) The Sundry Creditors were paid off less 3% discount.

(d) The realisation expenses incurred amounted to ₹ 1,200.

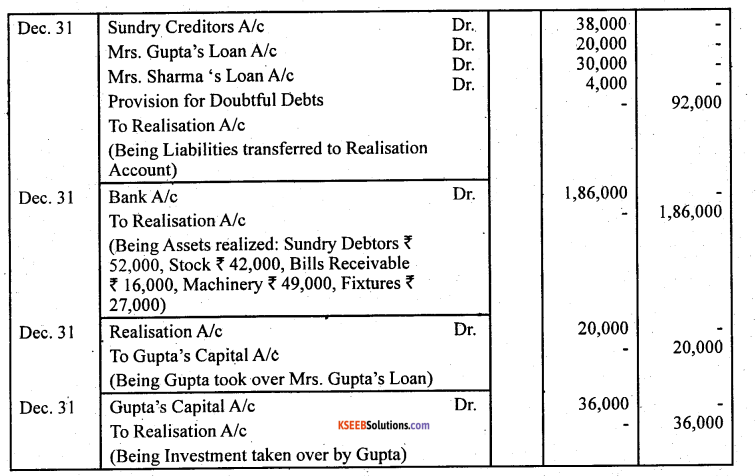

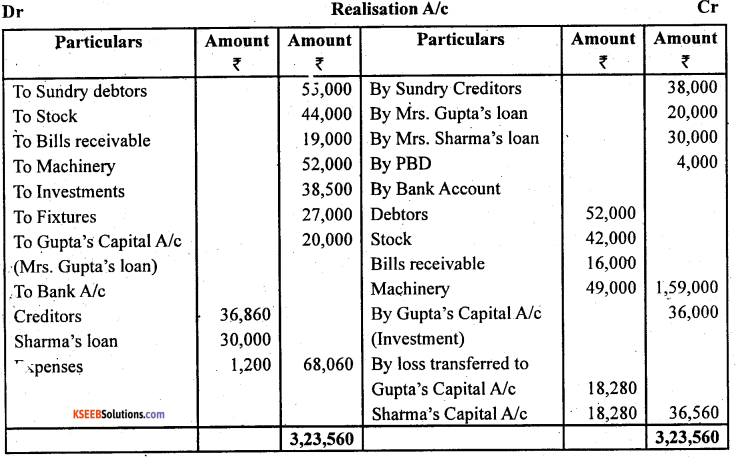

Journalise the entries to be made on the dissolution and prepare Realisation Account, Bank Account and Partners Capital Accounts.

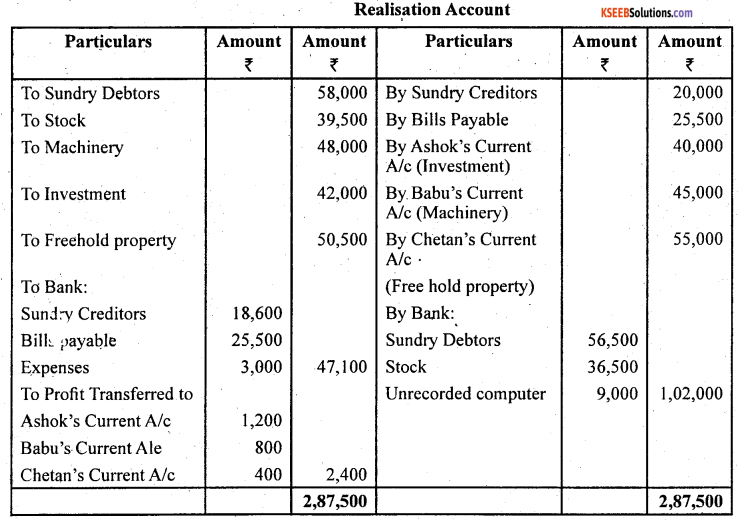

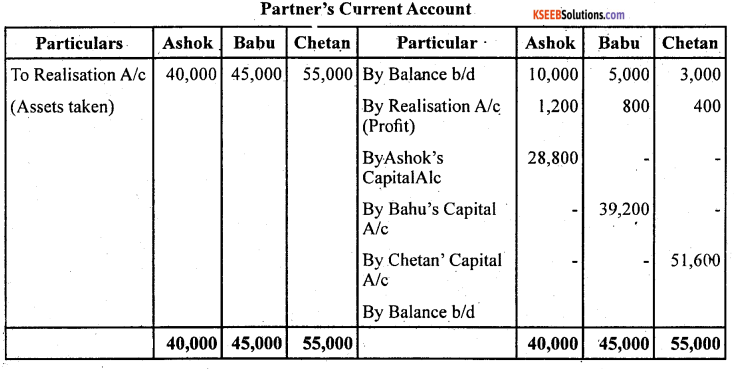

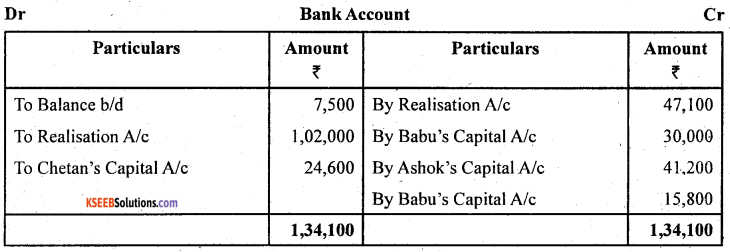

Answer:

![]()

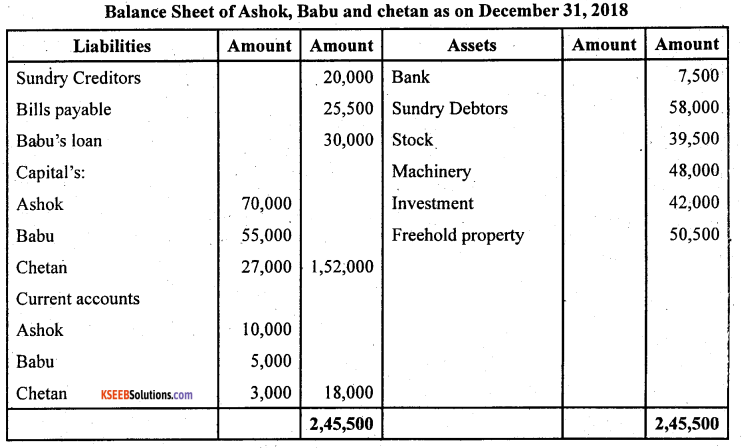

Question 19.

Ashok, Babu and Chetan are in partnership sharing profit in the proportion of 1/2. 1/3,1/6 respectively. They dissolve the partnership of the December 31, 2014 when the balance sheet of the firm as under:

The Machinery was taken over by Babu for ₹ 45,000, Ashok took over the investment for ₹ 40,000 and Freehold property took over by Chetan at ₹ 55,000. The remaining Assets realised as follows: Sundry Debtors ₹ 56,500 and Stock ₹ 36,500. Sundry Creditors were settled at discount of 7%. A Office computer, not shown in the books of accounts realised ₹ 9,000. Realisation expenses amounted to ₹ 3,000.

Prepare Realisation Account, Partners Capital Account, Bank Account.

Answer:

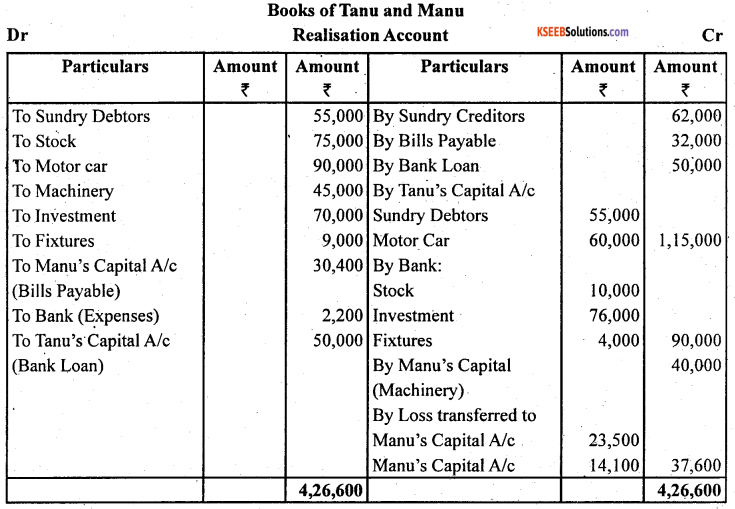

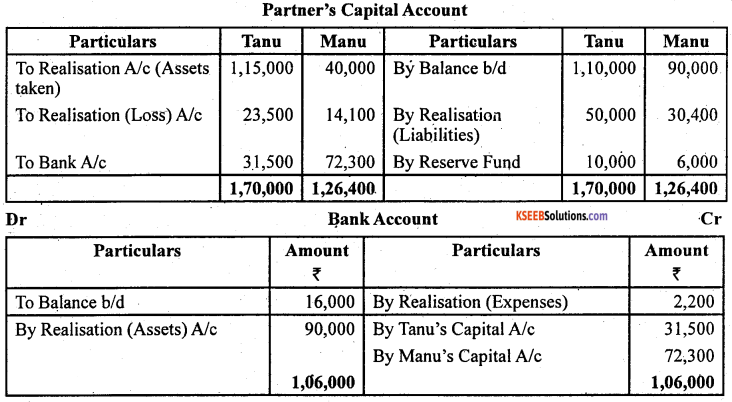

Question 20.

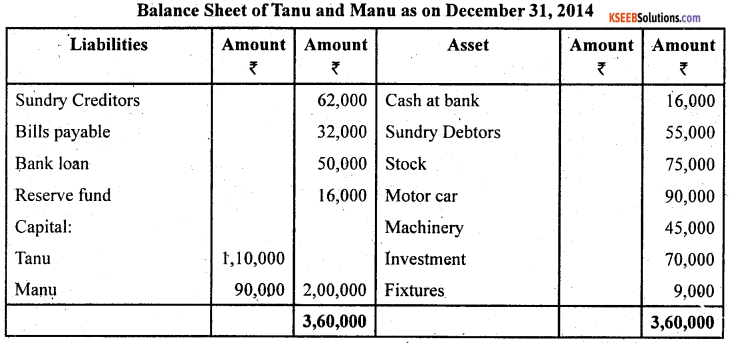

The following is the Balance sheet of Tanu and Manu, who shares profit and losses in the ratio of 5:3, On December 31,2014:

On the above date the firm is dissolved and the following agreement was made:

Tanu agree to pay the bank loan and took away the sundry debtors. Sundry creditors accepts stock and paid ₹10,000 to the firm. Machinery, is taken over by Manu for ₹ 40,000 and agreed to pay of bills payable at a discount of 5%. Motor car was taken over by Tanu for ₹ 60,000. Investment realised ₹ 76,000 and fixtures ₹ 4,000. The expenses of dissolution amounted to ₹ 2,200.

Prepare Realisation Account, Bank Account and Partners Capital Accounts.

Answer:

![]()